HKSFC Licensed Corp #ADC118

December Newsletter

Zhihaiquo completed more than 50 million US dollars in Series C financing

November 4, 2020

SCMP Webinar – Website Summary

November 20, 2020December Newsletter

MARKET UPDATE

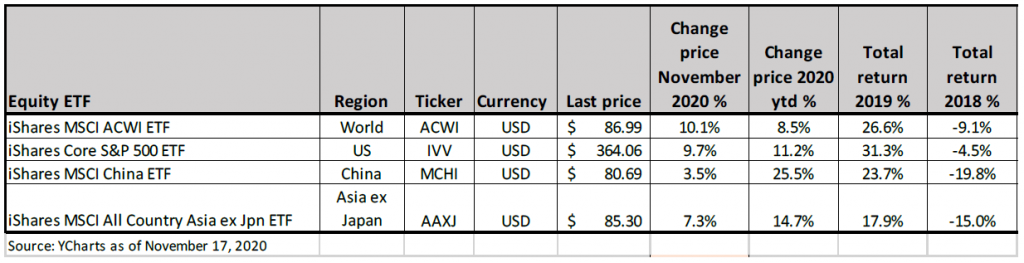

Equity market performance by region

Global Equity markets consolidated over September and October ahead of the US Presidential elections and as the Covid 19 health crisis continued. In November the markets have started strongly following the US elections and positive developments on a COVID 19 vaccination.

Despite the refusal of President Trump to concede defeat most investors expect that there will be a smooth transition of power to President elect Biden in January 2020. The markets also took comfort in the Republican party likely holding on to its majority in the Senate. This would reduce the threat of tax increases or major changes to US health care policies.

Pfizer Inc’s experimental COVID-19 vaccine is more than 90% effective based on initial trial results, the drug maker said on Monday, 9 November. Pfizer expects to seek U.S. emergency use authorization for people aged 16 to 85. Separately, Moderna announced on Monday, 16 November that it’s Covid – 19 vaccine shows nearly 95% protection. Subject to regulatory approval Pfizer and Moderna plan to deliver around 1 billion doses of the vaccine each in 2021.

It can be seen from the table below that most gains in the US and global markets for this year were registered in November. China remains the strongest major market in 2020, although it did not rally as strongly on the US election and vaccine news.

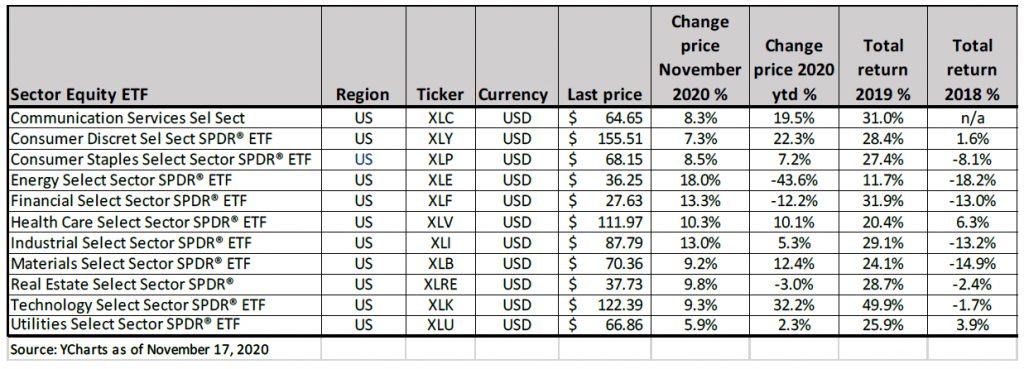

Equity market performance by sector

Following election night, the health care sector posted strong gains despite the likely win by Biden. That’s because Republicans are expected to maintain control of the Senate meaning that large scale changes in the regulation of the US health care sector is not expected. Energy, Financials, Industrials and Materials have all recorded double-digit gains in November. That is because of the encouraging news on the COVID-19 vaccine leading investors to chase sectors that are laggards, and which will benefit from a return to normal economic activity.

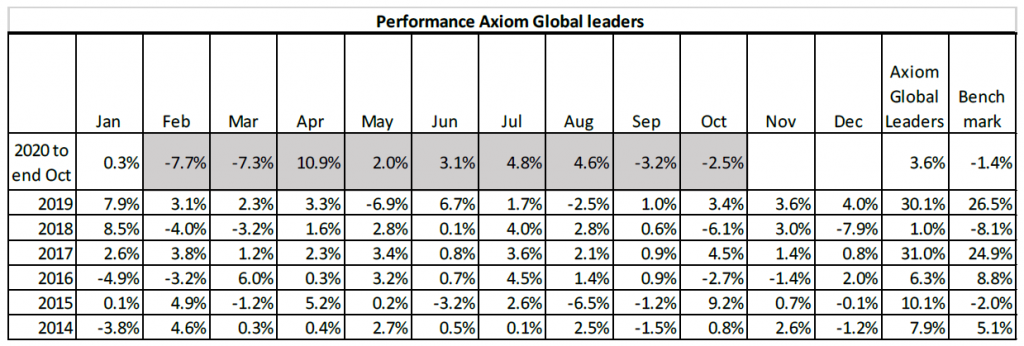

AXIOM GLOBAL SECTORS LEADERS PORTFOLIO REVIEW

The Axiom Global Sector leaders portfolio retreated in September and October in line with the market. The downside was protected slightly by the call options that we sold. Year to date the biggest gains have been recorded by Facebook, Alphabet, Tencent, Amazon, Alibaba, Apple, Microsoft, Semiconductor ETF and United Health Care. Negative returns were reported by China Construction Bank, JP Morgan and Merck. Losses were also recorded on Exxon and Boeing which have since been sold

We have made the following changes to the portfolio

Sold Lockheed Martin and purchased Honeywell

1) Likely victory for Biden means that defence spending growth may slow down over the next four years – this would negatively impact Lockheed

2) Honeywell has four divisions: Aerospace, Honeywell Building Technologies, Performance Materials and Technologies, Safety and productivity solutions. These should benefit from an economic pickup that should follow from a successful Covid 19 Vaccine

3) Honeywell is now the largest Industrial company globally so based on our process we should own the stock

4) Honeywell adjusted 2020 EPS is forecast to be down 14% on an adjusted basis – this is a solid performance given the economic sensitive nature of the business

Sell Puts on Alibaba, Apple and Facebook

The covered call option on Alibaba, Apple and Facebook that we previously sold was assigned on the call date. As we still like these stocks but consider the present levels high, we sold puts on quantities equivalent to our original positions.

performance based on model portfolio up to January 2020, from February 2020 onwards based on aggregate of actual portfolios

MARKET OUTLOOK

Going forward an effective Covid 19 vaccine is likely to be delivered in 2021. That would lead to the opening of economies and a gradual return to travel. This should lead to a recovery in this year’s laggard sectors being; Energy, Financial Services and Real Estate. Although Equity markets are expensive the very low interest rates mean that buying interest will remain. Overall, we are positive on Global equity markets in 2021.

All the information contained in this document is as of date indicated unless otherwise noted.

This document is issued by Axiom Investment Management Limited and has not been reviewed by the SFC. It may not be reproduced, distributed or transmitted to any person without express prior permission. This document and the information contained herein may not be distributed and published in jurisdictions in which such distribution and publication is not permitted.

Nothing contained here constitutes investment advice or should be relied on as such. The value of securities mentioned in the report and the income from it, if any, may fall or rise. Past performance of the securities mentioned in the report is not necessarily indicative of its future performance.

Axiom Investment Management Limited, Suite 3303, Singga Commercial centre, 144-151 Connaught Road West, Hong Kong. Telephone: 852 2537 2030 Facsimile: 852 2868-0091. Web: www.axiom-invest.com