HKSFC Licensed Corp #ADC118

September Newsletter

GMT Weekly Coaching with Alvin Ma

July 27, 2020

Mr. H

August 18, 2020September Newsletter

MARKET UPDATE

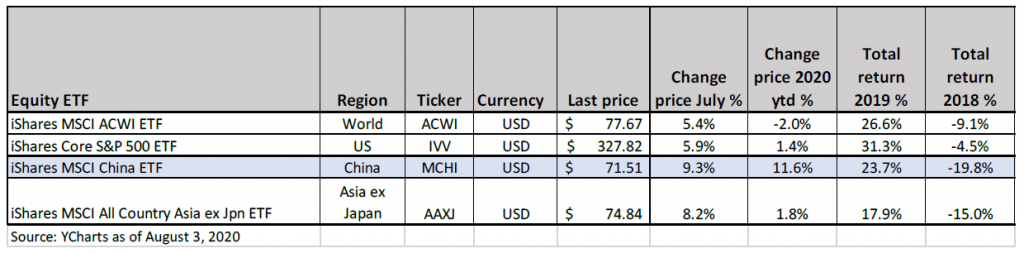

Equity market performance by region 2020

Global Equity markets reached a bottom on March 23 and since then have staged an

impressive recovery. In particular MSCI China which is up by 11.6% ytd. The US is also a

relative outperformer with the S&P500 increasing by 1.4% so far this year, whereas the MSCI

AC world index has declined by 2.0%.

There are several reasons that the markets have done well

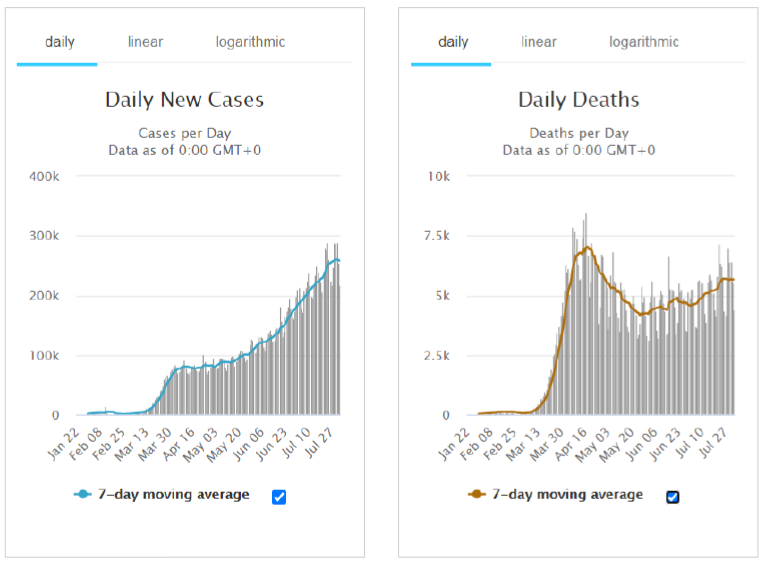

1) Although Covid 19 cases have continued to climb, more effective and earlier treatment

have made it a less fatal disease. On a 7-day moving average basis, mortalities peaked

on April 18 at 7,036 per day. It fell to 4,149 per day at the end of May. Although it has

started to climb again and is now 5,672 per day on a 7-day moving average basis, it

remains below the previous high. If fatalities don’t go beyond 7,000 per day, Covid 19

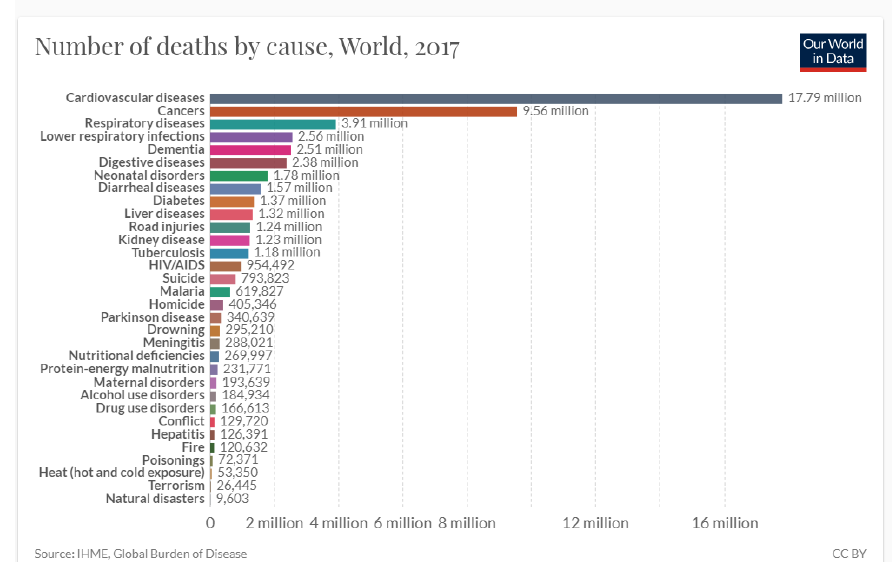

would become the fourth largest cause of death in the World at 2.6 million per year

behind Cardiovascular disease (17.8 million), Cancers (9.6 million), Respiratory

diseases (6.5 million). Although this would be a terrible result it would be something

which the global economies could cope with

Source: https://www.worldometers.info/coronavirus/

Source: Hannah Ritchie (2018) – “Causes of Death”. Published online at OurWorldInData.org. Retrieved from: ‘https://ourworldindata.org/causes-of-death’ [Online Resource]

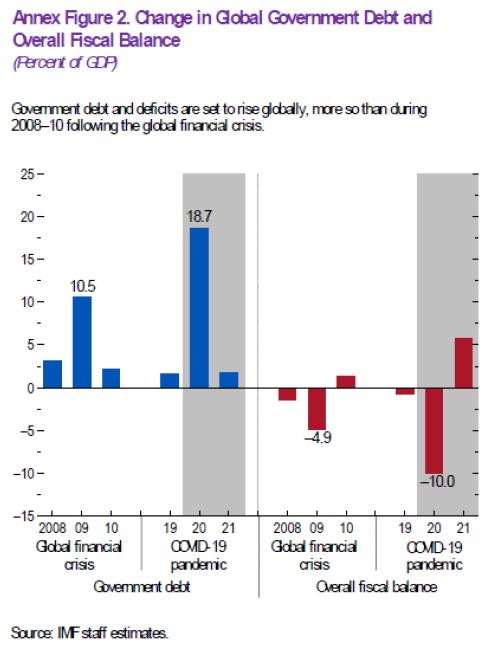

2) A massive fiscal boost enacted by Government’s globally. Announced fiscal measures globally are as of June 2020 were about USD11 trillion according to the IMF. One-half of these measures are additional spending and forgone revenue. The remaining half is liquidity support, such as loans, equity injections, and guarantees. As a result of this Government Debt globally is expected to increase to 18.7% of GDP in 2020, being far higher than the 10.5% recorded in 2009 after the Global Financial Crisis.

3) Massive easing of monetary policy

Federal funds rate: The Fed has cut its target for the federal funds rate, the rate banks pay to borrow from each other overnight, by a total of 1.5 percentage points since March 3, bringing it down to a range of 0 percent to 0.25 percent.

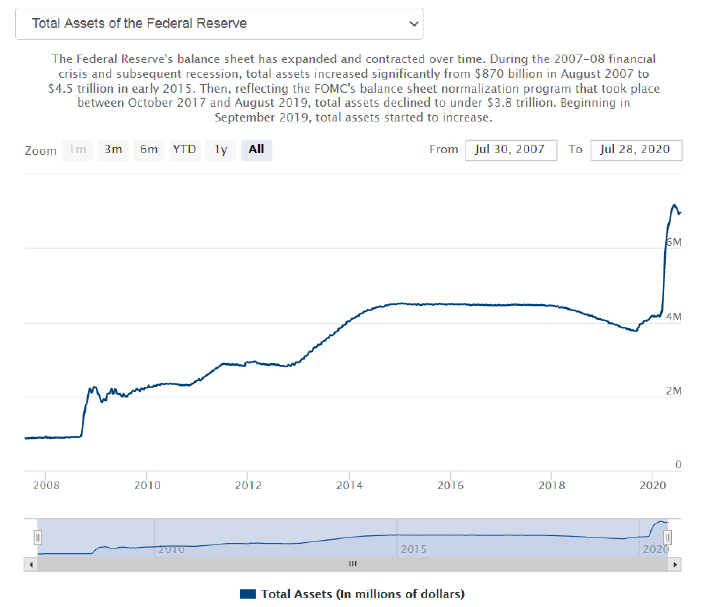

Securities purchases (QE): The Fed has resumed purchasing massive amounts of securities, a key tool employed during the Great Recession, when the Fed bought trillions of long-term securities. Treasury and mortgage-backed securities markets have become dysfunctional since the outbreak of COVID-19, and the Fed’s actions aim to restore smooth market functioning so that credit can continue to flow. Between mid-March and mid-July, the Fed’s portfolio of securities held outright grew from $3.9 trillion to $6.1 trillion. Source Brookings Institute

4) Many major economies e.g. China, Japan, Germany have controlled the spread of Covid 19, and economic activity is gradually recovering there. Even in the US there are signs that the economy is improving. The US economy notched its second straight month of job additions in June amid nationwide efforts to claw back from a coronavirus-induced recession. American businesses added 4.8 million nonfarm payrolls during the month, according to the Bureau of Labour Statistics. The US unemployment rate came in at 11.1%, the BLS said. It was also down from 13.3% in May. April’s 14.7% reading was the highest since the Great Depression of the 1930s. Source Business Insider

5) There is a global race to find effective cures and vaccines for Covid 19. There is debate over how effective they will be or when they can be deployed. However, overall Investors believe that Covid 19 will be contained by these new medicines and that we will be able to live with it – just like humans have with other illnesses

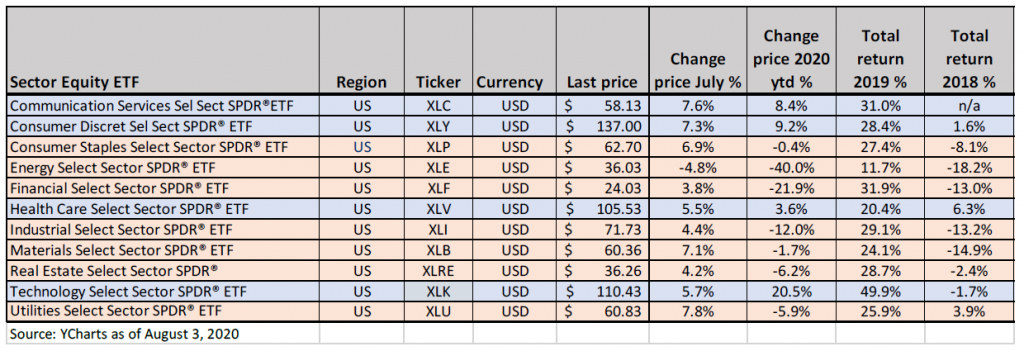

Equity market performance by sector 2020

For the month of July all sectors recorded gains except for Energy, which was down 4.8%. The Technology sector started the month weak as investors preferred to buy laggard sectors such as materials and utilities. However, it recovered towards the end of the month following strong Q2 earnings from Apple, Microsoft and most semiconductor companies. Sectors sensitive to economic activity underperformed. For example: Energy (low oil prices), Financials (higher loan loss provisions) and Industrials (collapse in commercial airplane demand). Despite the fall in interest rates sectors that should have stable earnings being: Utilities and Real estate have underperformed. This being due to worries that their earnings will be impacted by the economic downturn.

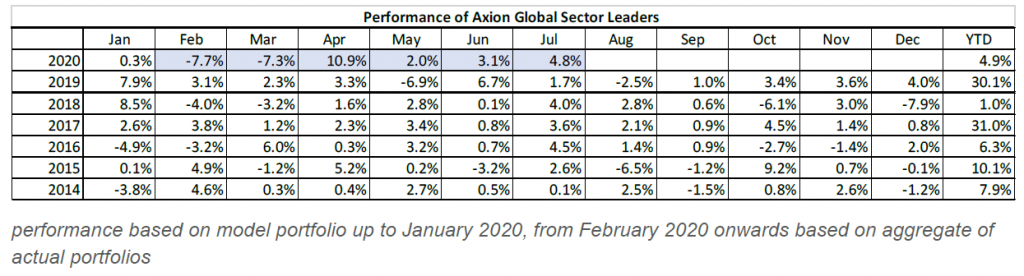

AXIOM GLOBAL SECTORS LEADERS PORTFOLIO REVIEW

Since the large market declines in February and March the Axiom Global Sector Leaders

Portfolio has recorded solid gains every month. For 2020 through to end July the portfolio is up by 4.9% outperforming the 1.2% decline in our benchmark, the iShare MSCI ACWI ETF. This

is due to the ownership of large cap stocks such as: Alibaba, Amazon, Apple, Facebook,

Microsoft and Tencent.

We have made the following changes to the portfolio

Sold Boeing and purchased Lockheed Martin.

Boeing is exposed to the commercial plane market which will be weak for some time. Also,

Boeing is now no longer the largest industrial globally. In purchasing Lockheed, we did not

follow our normal rule to buy the largest stock in a sector (it was the third largest). That is

because we though that its business of defence contracting would be relatively less impacted

by the economic downturn

Sold Exxon Mobil and purchased SAP SE

We decided to exit the energy sector as the fall in oil prices means that it is less important to

global equity indices (presently the weight in the iShare MSCI ACWI ETF is 3.2%). We chose

to add to the Information Technology sector which is a beneficiary of the Covid 19 economic

disruption and a long-term growth sector. We added SAP as its software products should help

companies transition to a more online business model. It is also the largest European software company so buying it helps us increase our exposure there.

Sold Intel and purchased iShares PHLX Semiconductor ETF

Following the disappointing announcement that Intel was to delay its next generation chips

until at least 2022 the market cap has fallen so that it no longer qualifies to be a global sector leader. We replaced it with iShares PHLX Semiconductor ETF. This is because we consider

that semiconductors remain a growth area. That’s because all new Technologies such as 5G,

AI and VR rely on a semiconductor to operate.

Sell covered call on part of positions in Alibaba, Apple, Facebook, Microsoft and United Health

Following the strong rises in these stocks we decided to monetize some of our gains by selling at the money covered calls on part of our stock positions. This enabled us to receive premium of over 5% on those positions

Rebalance by taking partial profit on the Amazon position.

MARKET OUTLOOK

Going forward the market could have short term setbacks as the pace of economic recovery is likely to decline due to increased Covid 19 infection rates. However, these should be regarded as buying opportunities. That is because we think that the disease can be contained within the next 12 months meaning that the Global economy will return to a growth path by 2021.

All the information contained in this document is as of date indicated unless otherwise noted.

This document is issued by Axiom Investment Management Limited and has not been reviewed by the SFC. It may not be reproduced, distributed or transmitted to any person without express prior permission. This document and the information contained herein may not be distributed and published in jurisdictions in which such distribution and publication is not permitted.

Nothing contained here constitutes investment advice or should be relied on as such. The value of securities mentioned in the report and the income from it, if any, may fall or rise. Past performance of the securities mentioned in the report is not necessarily indicative of its future performance.

Axiom Investment Management Limited, 25/F, 168 Queen’s Road Central, Hong Kong. Telephone: 852 2537 2030 Facsimile: 852 2868-0091. Web: www.axiom-invest.com