HKSFC Licensed Corp #ADC118

2020 3-4Q Portfolio Rebalancing in view of Sino-US geo-political concerns & US Election Era

2020 1H Global Asset Allocation Portfolio Review

July 9, 2020

GMT Weekly Coaching with Alvin Ma

July 27, 20202020 3-4Q Portfolio Rebalancing in view of Sino-US geo-political concerns & US Election Era

CMT Zoom Conference

Table of Content

A. Macro Factors & Investment Outlook:

i. Cause & Effect

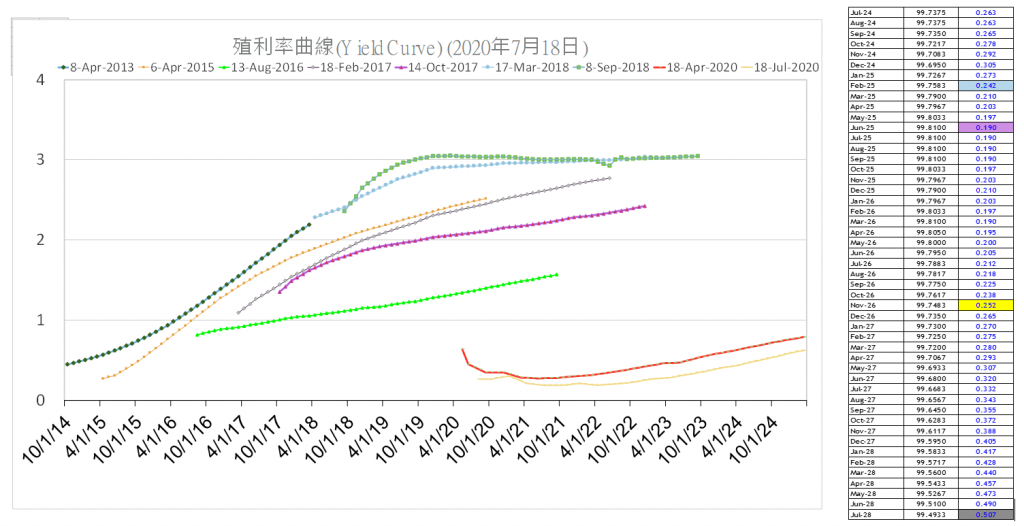

a. USD interest rates at historical sub-zero low……

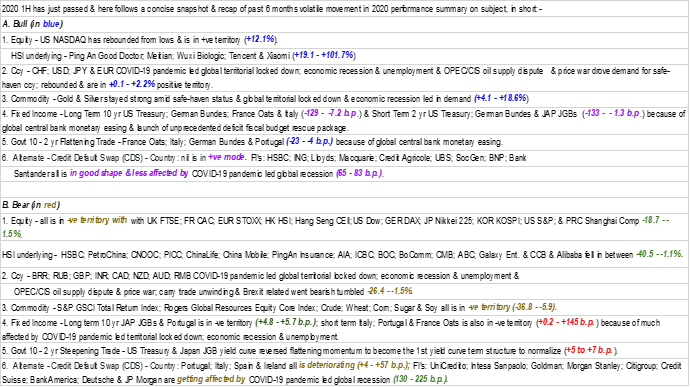

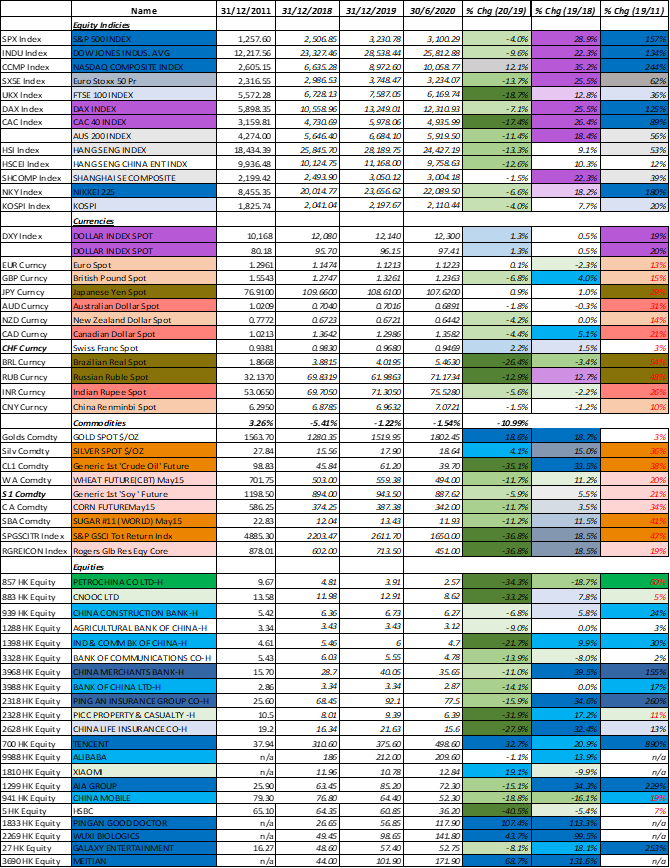

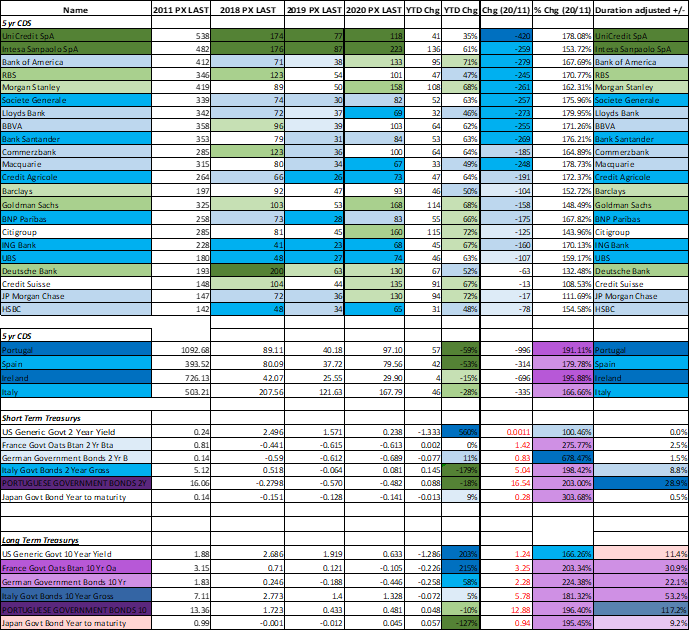

b. Global Asset Allocation Performance Summary:

c. Big mkt turning point between Mar 12 (VIX at highest) n Mar 16 when US Fed established MMF Liquidity Facility to stabilize the Markets..

“Asset Management under COVID-19 – July 7 2020 by Dr. King Au, Chief Executive of Value Partners”

d. Vaccine at 3rd stage n approval to be secured soonest!

Mostly likely 2 from PRC, 1 each from Germany n UK.

ii. Effect & Implications

Forward into Nov US Election n Sino US intensive conflicts n deepening Central Banks’ QE in face of recession if not depression, how shud one position one’s portfolio n allocation strategies….?

B. Discussion focal points:

- outlook of the possible currency war,

- possible outcome of massive QE,

- removal of USD as reserve currency for RMB and

- direct conflict of RMB versus USD,

- possible future scenario, how likely are they and what’s the impact.

C. Implications for CNY to be de-dollarized

D. HKD as an exchange & medium ccy

E. Alternate CNY & HKD based asset diversification & allocation

– Different investment vehicles for hedging against this risk

1. Gold,

2. Commodity like oil n gas

3. CNY/TUL; CNY/UAD; CNY/IRP….

4. all via barter trades with the underworld without passing/transacting thru USD, n it’s been ongoing since 2017, but more so now.

F. Global Investment Outlook

Gold has hit beyond usd1800 since Jul 7 n is now at usd1816 high targeting usd2,200 in coming 5 month.

Macro outlook is volatile in coming 5 mons in medium term.

G. Alternate asset diversification & allocation

All are alternate Investment strategies to diversify away from main-stream asset underlying volatilities.

A. Stay away from Equity, FX (USD is one & only safe haven ccy) n Money Market (cash) as its yielding zero….

B. Engage yield enhancement strategies as Core….by locking into 4-5% 2 yr short duration usd high yield bond.

C. Sell covered calls (pls refer to Appendix) on all FAANG n ANTES stocks so as to yield enhance for the equity portfolio.

D. Sell low delta (5-10%) protective puts (pls refer to Appendix) on all -30% plus cyclical n cashflow equities such as big banks, telecoms, retail n property conglomerates looking for rebound n if not yield enhancement

E. Buy OTM low delta calendar calls on Gold, Silver m Palladium

F. Open Type 1 Investment ac in GZ PRC banks to secure 4% p.a. wealth mgmt cash equiv. products

G. Engage into PRC Healthcare n Fintech A shares ETFs n Public Funds.

H. GBA WM Connect North (RMB) /South (HKD/USD) Bound channel is in…

i. Top 10 PRC PWM banks

ii.https://www.scmp.com/business/banking-finance/article/3092655/who-wins-who-loses-chinas-plans-greater-bay-area-wealth

….as explained in Goldman Sachs research n analysis

ii. Core Affluent PWM is meant for this bracket (RMB500k to 3mio).

iii. Among the Top 10 rankings.

- For WM solutions.

- Listed Mutual Fund opportunity wise even is bigger n wider.

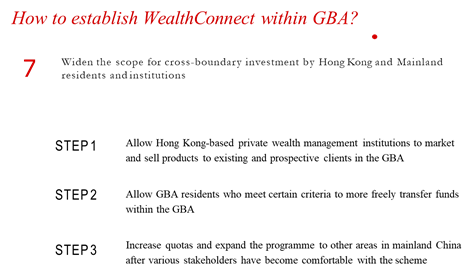

iv. Cross-boundary Wealth Management Connect (WMC) Scheme for Greater Bay Area (GBA)

1) NEW business environment after WMC effective

2) Cross-boundary remittance channel

a. Southbound Vs. Northbound

b. Closed-loop

3) The extensions of WMC

a. Product Management and Innovation for WMC

b. Importance of Customer Suitability

c. Needs of WM Expertise and Profession

I. GBA WM Connect WM Solutions…

For WM solutions I will recommend multiple bar bell allocations onto both short term 3 month n medium term 12 month deposits n index linked (CSI 300/SHSZSE 300/XAU/FX…) structured products.

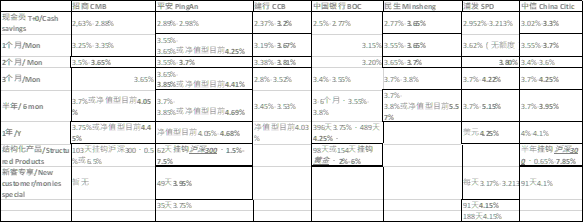

1. 3 month deposits as newly joined clients with joint stocks ownership banks such as SPD, PingAn n China Citic at 4.25% p.a.

2. 12 month 50% net value based(淨值形) at 4.45% p.a. n 50% 180 days SH/SZ A shares index linked structured deposits at 0.65-7.85% p.a.

avg 2.25-6.15% p.a.

3. Portfolio wide avg 3.75-6.05% p.a.

In summary PRC WM Connect North Bound has enormous opportunities.

4. Overview of RMB funds –

a. Market performance

b. Performance of domestic public offering funds (equity inclined type)

c. Performance of domestic public offering funds (debt inclined)

d. That Northbound WM n AM opportunities.

e. Southbound will be HKMA/SFC accredited ELI, DCI, FX structured products, Accredited mutual funds n Fund Linked Elis….

Pls take a look at the above as I have recently made various presentations on RMB as replacement investment ccy underlying for both USD n HKD.

Appendix

1.Launch of the Cross-boundary Wealth Management Connect Scheme in the Greater Bay Area – KPMG

2. Option trading with underlying assets

a. Covered Calls

b. Protective put

A. Macro Factors & Investment Outlook:

i. Cause & Effect

USD interest rates at historical sub-zero low……

Global Asset Allocation Performance Summary:

Fresh from Dr. King Au, CE of Value Partners.

Big mkt turning point between Mar 12 (VIX at highest) n Mar 16 when US Fed established MMF Liquidity Facility to stabilize the Markets..

“Asset Management under COVID-19 – July 7 2020 by Dr. King Au, Chief Executive of Value Partners”

“Bond Market Liquidity Crunch

- Bonds are considered a relatively safe and defensive asset class !

- Why did the global bond markets come close to a melt down in March?

- Bonds held up much better than equity until March when liquidity suddenly dried up!

- 9 Mar: The onset of an all-out price war between Saudi Arabia and Russia was the straw that broke the camel’s back

- The scramble for cash caused dislocations even in government bonds!

- It all started with a stampede in Prime Money Market Funds (mainly short-term corporate debt

with maturities of a few days to a year) in the US.

Flight to Quality

- Default concerns prompted investors to switch from Prime MMFs and Corporate Bonds to UST in early March (~USD 800bn inflow by end of March!)

- Managers rolling longer dated assets into shorter maturity papers to preserve liquidity and avoid gating!

- 12 March: Primary market liquidity dried up as market makers reaching balance sheet and market risk limits

- 15 March: Fed introduced a large purchase program of UST and agency mortgage-backed

securities to clear market makers’ risk-taking capacity

- 18 March: Fed established MMF Liquidity Facility to stabilize the Prime MMFs

Unintended Consequences

- Massive outflow from Prime MMFs caused short-term funding difficulties for banks and a significant shortening of funding maturities! The severity was to the extent that many foreign banks had problem accessing USD repos on black Friday, the 13 March

- Prime MMFs, with floating NAV, has a 30% liquid asset limit (T-bills and 7 days maturity papers). If it is breached then an exit fee up to 2% and/or gating for 10 days can be imposed. If weekly liquidity falls below 10% then a 1% liquidity fee is required unless waived by the fund board

- Prime MMFs suffered 15% AUM outflow from 2 to 23 March to the tune of USD 120b. A vicious cycle of selling triggered by institutional investors trying to get out of MMFs before the liquidity penalties kick in

- Unlike the GFC in 2008, non-bank financial institutions were at the epicentre of the liquidity

squeeze and banks were collateral damages this time

- The introduction of MMLF on 18 March did stabilize the MMFs but accentuated the selling of credits unintentionally!

- The global high yield bond market came close to a melt-down in the week of 16 March due to

deleveraging by financial intermediaries which led to high profile fund gating and closures….

Did ETFs pass the stress test?

- Even the world’s largest bond ETFs traded at huge discounts to NAV,

i.e. >5% for IG and > 9% for HY

- Two large spikes in NAV discounts happened on 12 and 19 of March!

- 12 March: Primary market liquidity dried up as market makers reaching balance sheet and market risk limits. Authorized Participants (AP) came under pressure in times of market distress to produce “one way” secondary market liquidity which compounded the selling pressure in a falling market.

- 18 March: Fed established MMF Liquidity Facility to stabilize the Prime MMFs. This prompted investors to switch from IG Bond ETFs to MMFs

- 23 March: Fed came to the rescue as a lender of last resort again with “unlimited” purchases of individual IG bonds and IG ETFs “as needed”

Lessons learnt

- Key risk indicators need to be global and timely

- Asset class diversification cannot be taken for granted over short time frames

- Liquidity Premium and Investment Horizon do go hand in hand

- Excessive leverage should be discouraged and risk disclosure does not exonerate our fiduciary

duties to clients

- Should some of the largest funds or their managers be classified as systemically important financial institutions (SIFI)?

- More liquidity management tools required, e.g. Swing Pricing”

Rationale behind US Fed QE n CP buyback on Mar 18 for a Big U-Turn on US equity mkts orchestrated by Trump/Mnuchin for re-election purpose which is not sustainable….

Both Black People Lives n Uncontrolled Covid-19 pandemic post market re-opening will cost him n the Republicans their next 4 yr political role. Stay away from USD n US equity market at this historical high point n depression will sink their ships.

https://ca.finance.yahoo.com/news/huge-market-crash-coming-warren-121015499.html

Stay acute n profit take if one can….👍😎

“Huge Market Crash Coming? Warren Buffett and Other Experts Sound the Alarm

Billionaire investors are parading and sounding the alarm on the coming of a massive market crash. The GOAT of investing is leading the parade of the wealthy. Warren Buffett is supposed to be deploying cash in a declining market, but he isn’t.

People find it odd that Buffett has lost his investment appetite in 2020. His conglomerate has $137 billion in the treasure chest……………

Induced hallucinations

People are staying home due to COVID-19 and are playing stock market. The contrarian moves of these amateurs worry Buffett. He doesn’t like the mindless buying and speculating. Day traders, especially, are scooping up shares of distressed companies.

The day-trading boom at present has similarities with the dot.com bubble in early 2000. Buffett said that investors are focusing “not on what an asset will produce but rather on what the next fellow will pay for it.”

Market bubble will burst

NBA personality and owner of the Dallas Mavericks franchise Mark Cuban shares Buffett’s sentiment. He believes the stock market’s breathless rally will end once the magnitude of the pandemic’s devastation is known. Day traders are making money thinking they are geniuses in a bull market.

Howard Marks, another billionaire investor and CEO of Oaktree Capital in the U.S., said people are buying stocks for fun. Don’t look at it as a gambling game because reckless trading is not healthy. Many thought during the dot.com era, it was a “can’t miss strategy.” The bubble eventually burst.

Defensive stop in a falling market

The purchase of Dominion Energy assets by Berkshire indicates Buffett’s move toward pure-play state-regulated, sustainability-focused utility operations. There is a utility stock on the TSX that makes for the same attractive investment option.

Top choice of exposure in the utility sector. regulated electric company has bond-like features but offers higher returns. One’ll be investing in a long-term dividend play.

During recessions, investors look for defensive stocks. The business of Fortis will endure economic meltdowns, including the current health crisis. It is a well-diversified and acknowledged leader in North America’s regulated electric and gas utility industry.

Reality will set in

The billionaire wannabes are gambling, not investing. Buffett, Cuban, and Marks are warning investors not to get carried away. Now is not the time for speculating because the market is standing on thin ice.

When a pullback happens, it will trigger a severe sell-off as people will yank out their money from the market.

The post Huge Market Crash Coming? Warren Buffett and Other Experts Sound the Alarm appeared first on The Motley Fool Canada.”

Vaccine at 3rd stage n approval to be secured soonest!👍😎

Mostly likely 2 from PRC, 1 each from Germany n UK.

ii. Effect & Implications

Indeed n very truthful….majority is playing on fire n all fundamental data do not justify that….

Forward into Nov US Election n Sino US intensive conflicts n deepening Central Banks’ QE in face of recession if not depression, how shud one position one’s portfolio n allocation strategies….?🤗👍😎

B. Discussion focal points:

- outlook of the possible currency war,

- possible outcome of massive QE,

- removal of USD as reserve currency for RMB and

- direct conflict of RMB versus USD,

- possible future scenario, how likely are they and what’s the impact.

C. Implications for CNY to be de-dollarized

Like the Bond one, for what to invest in this era of possible currency become worthless

An introduction to investments like Gold, or anything that can hedge against the devaluation of currency

The USD ccy leg being discontinued will be challenging n disastrous….

If RMB removes USD, USD will be worthless, but RMB will be worthless as well

So will HKD, so that is a good investment to hedge against this risk

Affirmative as both will be hard hit n devastating, but PRC has already looked for her alternate scenarios since 2017…

D. HKD as an exchange & medium ccy

HKD is now ready to diminish/transited via CNH overnite like that of Macau Dollar…

HKD is not an intl exchange medium.

E. Alternate CNY & HKD based asset diversification & allocation

– Different investment vehicles for hedging against this risk

1. Gold,

2. Commodity like oil n gas

3. CNY/TUL; CNY/UAD; CNY/IRP….

4. all via barter trades with the underworld without passing/transacting thru USD, n it’s been ongoing since 2017, but more so now.

F. Global Investment Outlook

Gold has hit beyond usd1800 since Jul 7 n is now at usd1816 high targeting usd2,200 in coming 5 month.

Macro outlook is volatile in coming 5 mons in medium term.

G. Alternate asset diversification & allocation

All are alternate Investment strategies to diversify away from main-stream asset underlying volatilities.

A. Stay away from Equity, FX (USD is one & only safe haven ccy) n Money Market (cash) as its yielding zero….

B. Engage yield enhancement strategies as Core….by locking into 4-5% 2 yr short duration usd high yield bond.

C. Sell covered calls (pls refer to Appendix) on all FAANG n ANTES stocks so as to yield enhance for the equity portfolio.

D. Sell low delta (5-10%) protective puts (pls refer to Appendix) on all -30% plus cyclical n cashflow equities such as big banks, telecoms, retail n property conglomerates looking for rebound n if not yield enhancement

E. Buy OTM low delta calendar calls on Gold, Silver m Palladium

F. Open Type 1 Investment ac in GZ PRC banks to secure 4% p.a. wealth mgmt cash equiv. products

G. Engage into PRC Healthcare n Fintech A shares ETFs n Public Funds.

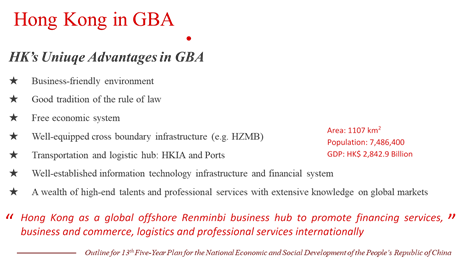

H. GBA WM Connect North (RMB) /South (HKD/USD) Bound channel is in…

Top 10 PRC PWM banks…

….as explained in Goldman Sachs research n analysis….

Who wins, who loses in China’s plans for a Greater Bay Area wealth management hub? Banks with large retail market share on the mainland and offshore likely to be beneficiaries. Boutiques, brokers and insurance companies have seen missing out.

Banks that straddle China’s borders look set to be the major beneficiaries of a new wealth management scheme catering to over 70 million people living in the Greater Bay Area.

Meanwhile, private banking boutiques, brokers and insurance companies are effectively barred from selling products via the scheme, dubbed Wealth Management Connect, according to regulators and industry professionals.

China’s outline of the Wealth Management Connect pilot project, unveiled on June 29, was short on detail.

But regulators and industry professionals’ working plan is that only banks with a partner on the other side of the border will be eligible to sell wealth management products under the scheme, people familiar with the matter said.

Hong Kong can benefit from the closer economic collaboration with the bay area, said Peter Wong, the deputy chairman and chief executive of Hongkong and Shanghai Banking Corporation Ltd, a unit of HSBC Plc. “We are already prepared for mainland investors to open mutual fund and investment accounts in Hong Kong,” said Wong.

HSBC is present in all 21 prefecture-level cities in Guangdong, and more than a third of its outlets in mainland China are located in the Guangdong Province.

Financial institutions such as Bank of China, London-headquartered HSBC and Bank of East Asia (BEA) will be in a strong position as they have operations in both Hong Kong and the mainland, said Bruno Lee, chairman of the Hong Kong Investment Funds Association.

For most banks, selling wealth management products in the bay area represents a growth opportunity at a time when business is flagging because of the economic fallout from the coronavirus and anti-government protests.

“BEA is well positioned to serve the different investment needs of our customers in the region,” said Adrian Li Man-kiu, co-chief executive of BEA. BEA has 75 branches in Hong Kong and 25 branches in the nine cities in the bay area.

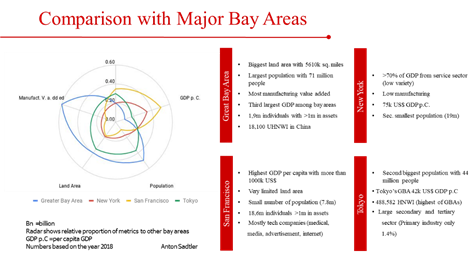

The bay area is one of the world’s largest banking clusters with revenues expected to reach US$185 billion by 2025, a 10.3 per cent compound annual growth rate, according to analysis by HSBC.

Hong Kong’s investors are likely to be more active users of the Wealth Management Connect than mainlanders, at least initially, said analysts.

Fixed income products are likely to be most in demand, given the widening interest rate spread versus offshore wealth management products. As the global hunt for yield accelerates with most of the developed world’s interest rates around zero, mainland China’s fixed-income wealth management products are looking increasingly attractive.

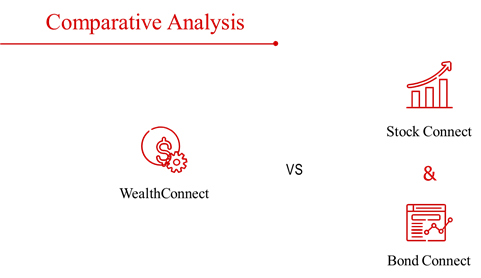

Hong Kong investors already have access to the mainland’s equity markets via a mutual recognition scheme called Stock Connect, but the fixed-income equivalent, Bond Connect is reserved for institutional investors only.

This again puts banks such as HSBC and Bank of China (Hong Kong) in strong positions, as both have strong debt franchises and can work with their mainland China businesses to distribute products.

Foreign banks from 13 countries and regions had established a total of 155 business institutions in Guangdong province, excluding Shenzhen, as of February.

Goldman Sachs analysts highlighted China Merchants Bank and Ping An Bank, both headquartered in Shenzhen, as retail banks with strong networks in Guangdong. Both also have branches in Hong Kong. Privately owned banks had a 41 per cent share of mainland China’s US$3 trillion market of wealth management products as of June last year, more than 37 per cent commanded by the large state-owned banks, Goldman Sachs said. The market on the mainland is heavily skewed towards fixed-income products.

The flip side of this neat arrangement is that banks without a partner in China are at a disadvantage. Boutique private banking players with no mainland partner, for example, could struggle to capitalise on the scheme.A European private boutique bank executive, who declined to be named, said the scheme would be of little benefit to small private banks which have a limited presence in mainland cities.

He also said the scheme was unappealing for his clients as it does not allow mainlanders to remit funds outside Hong Kong. Once the clients sell an investment made via the scheme, the money must return to the mainland. This also means financial firms not covered by the plan will not be able to capture any funds indirectly.

Private banking and wealth management boutiques with a presence in Hong Kong include Swiss-headquartered Pictet and Lombard Odier, as well as Liechtenstein-based LGT.

Smaller private banks could still seek a tie-up with a firm in the bay area, said Lee.

Also, regulators’ emphasis on purely plain vanilla products means the scheme is likely to be less relevant to the largest private banking firms. Swiss banks UBS and Credit Suisse serve billionaires with products at the more complex and riskier end of the range.

Insurance companies are also unlikely to get a windfall from the Wealth Management Connect scheme. Savings-oriented insurance products probably won’t be included in the scheme, said analysts.

“It’s unlikely to include regular premium policies, as it would require significant annual expansion of fund flow quota,” said Thomas Wang, an analyst at Goldman Sachs.

The Wealth Management Connect scheme differs from the Stock and Bond Connects in that distribution is via banks only – meaning this time brokerage houses will also miss out.

The more than 600 stockbrokers in Hong Kong were disappointed, according to Tom Chan Pak-lam, chairman of the Hong Kong Institute of Securities Dealers.

“We want to urge the Hong Kong government to urge the mainland authorities to expand the sale points to brokers,” Chan said.

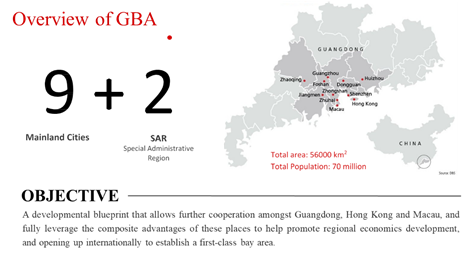

Core Affluent PWM is meant for this bracket (RMB500k to 3mio).

Among the Top 10 rankings.

For WM solutions.

Listed Mutual Fund opportunity wise even is bigger n wider.

Cross-boundary Wealth Management Connect (WMC) Scheme for Greater Bay Area (GBA)

1) NEW business environment after WMC effective

2) Cross-boundary remittance channel

a. Southbound Vs. Northbound

b. Closed-loop

3) The extensions of WMC

a. Product Management and Innovation for WMC

b. Importance of Customer Suitability

c. Needs of WM Expertise and Profession

I. GBA WM Connect WM Solutions…

For WM solutions I will recommend multiple bar bell allocations onto both short term 3 month n medium term 12 month deposits n index linked (CSI 300/SHSZSE 300/XAU/FX…) structured products.

1. 3 month deposits as newly joined clients with joint stocks ownership banks such as SPD, PingAn n China Citic at 4.25% p.a.

Absolutely for yield pick up of 2% p.a. more.

Much better than HK based WM solutions if 1.7% p.a best.

2. 12 month 50% net value based(淨值形) at 4.45% p.a. n 50% 180 days SH/SZ A shares index linked structured deposits at 0.65-7.85% p.a.

avg 2.25-6.15% p.a.

3. Portfolio wide avg 3.75-6.05% p.a.

| 评估对 – 整体理财产品收益率,股份制行>国有银行 |

| Peer comparison: overall financial product yield, joint-stock banks>state-owned banks |

In summary PRC WM Connect North Bound has enormous opportunities.

Overview of RMB funds -人民币基金概览

- 市场表现

1. Market performance

| 近一月涨幅 1 mon Performance | Top 10 | 今年涨幅 Y-T-D Performance | Top 10 | 近一年涨幅 1Y Performance | Top 10 | 市值前十 Top 10 by mkt cap |

| 券商信托 Brokerage / Trust | 25.75% | 医疗 Medical Treatment | 75.86% | 医疗 Medical treatment Electronic component | 90.57% | 银行 Bank |

| 医疗 Medical Treatment | 18.53% | 医药制造 Pharmaceutical Manufacturing | 30.16% | 电子元件 Electronic Component | 45.63% | 医药制造 Pharmaceutical Manufacturing |

| 酿酒 Winemaking | 16.87% | 食品饮料 Food and Beverages | 29.74% | 玻璃陶瓷 Glass Ceramic | 38.42% | 电子元件 Electronic Component |

| 保险 Insurance | 15.13% | 电信运营 Telecom Operators | 27.86% | 医药制造 Pharmaceutical Manufacturing | 37.68% | 酿酒行业 Winemaking |

| 医药制造 Pharmaceutical Manufacturing | 12.52% | 材料行业 Material Industry | 22.14% | 电子信息 Digital Information | 34.83% | 券商信托 Brokerage / Trust |

| 多元金融 Diversified Finance | 11.96% | 农牧饲渔 Farming, Animal Husbandry, Feeding & Fishing | 22.00% | 食品饮料 Food and Beverages | 34.24% | 保险 Insurance |

| 玻璃陶瓷 Glass Ceramic | 11.56% | 酿酒 Winemaking | 20.73% | 软件服务 Software Service | 31.49% | 软件服务 Software Service |

| 煤炭采选 Coal Mining | 10.31% | 塑胶制品 Plastic Products | 20.55% | 塑胶制品 Plastic Products | 28.32% | 房地产 Real Estate |

| 房地产 Real Estate | 8.94% | 专用设备 Professional Facilities | 20.31% | 材料行业 Material Industry | 25.69% | 汽车行业 Automobile Industry |

| 电信运营 Telecom Operators | 8.60% | 软件服务 Software Service | 18.85% | 专用设备 Professional Facilities | 25.64% | 医疗 Medical treatment |

从指数来看,最近一年以及今年上半年都有不错的上涨,尤其创业板和中小板涨幅明显。从行业来看,最近一年以及今年上半年医疗行业涨幅最大,酿酒和食品饮料也取得持续增长。

From the index point of view, the recent year and the first half of this year have had a good rise, especially the growth of the ChiNext and Small & Medium-sized Boards. From an industry perspective, the medical industry saw the largest increase in the past year and the first half of this year, and wine and food and beverages also achieved sustained growth.

二.国内公募基金表现(偏股型)

Wind数据,今年上半年

2. Performance of domestic public offering funds (equity inclined type)

WIND data, the first half of this year

| 主动管理股票型基金 Actively managed equity funds | 混合型基金 Hybrid fund | 指数型 Index linked | 多空对冲 Long-short hedge | ||||

| 同类平均 | 26.09% | 同类平均 | 16.66% | 同类平均 | 9.31% | 同类平均 | 6.14% |

| 创金合信医疗 | 83.71% | 融通医疗保健 | 73.68% | 招商国证生物医药 | 66.03% | 富国绝对收益多策略 | 12.24% |

| 广发医疗保健 | 77.94% | 融通健康产业 | 70.07% | 易方达生物科技 | 65.39% | 中邮绝对收益 | 10.75% |

| 宝盈医疗健康 | 75.84% | 中信建投医改 | 69.12% | 国泰中证生物医药ETF | 61.37% | 工银瑞信绝对收益 | 9.97% |

| 工银瑞信前沿医疗 | 75.96% | 南方医药保健 | 68.32% | 汇添富中证生物科技A | 60.76% | 中金绝对收益 | 6.50% |

| 工银瑞信养老 | 74.27% | 中欧医疗健康 | 67.63% | 华宝中证医疗ETF | 60.68% | 安信稳健阿尔法 | 6.48% |

| 医疗基金行业平均 Peer Avg. | 52.56% | 消费基金行业平均 Peer Avg. | 24.82% | 科技基金行业平均 Peer Avg. | 33.00% | 农业基金行业平均 Peer Avg. | 28.30% |

今年上半年对于偏股型基金来看,选对行业即会取得不错回报,而根据wind行业板块评估,目前存在低估的行业板块为:保险,银行,互联网,基建工程,农业,地产,建筑材料,军工。

除了短期可参考板块选择行业基金以外,中长期稳定增长的基金也可作为参考,中长期业绩看:

For equity inclined funds in the first half of this year, choosing the right industry will achieve good returns. According to the assessment of the WIND industry sector, the currently undervalued industry sectors are: insurance, banking, internet, infrastructure engineering, agriculture, real estate, building materials , & military & defence industry.

In addition to short-term reference sector selection of industry funds, medium and long-term stable growth funds can also be used as a reference, in terms of mid- and long-term performance:

| 基金排名Fund ranking | 近三年收益 3Y Performance | 近五年收益率 5Y Performance | 近十年收益 10Y Performance | ||

| 行业平均 Peer Avg. | 43.26% | 行业平均 Peer Avg. | 33.95% | 行业平均Peer Avg. | 169.64% |

| 中欧医疗健康 | 179.10% | 万家行业优选 | 201.99% | 华泰柏瑞价值增长 | 517.12% |

| 交银医药创新 | 178.83% | 前海开源国家比较优势 | 172.29% | 兴全合润分级 | 503.74% |

| 宝盈鸿利收益 | 175.47% | 银华富裕主题 | 161.33% | 银河行业优选 | 473.25% |

| 富国新动力 | 172.98% | 南方医药保健 | 152.04% | 汇添富民营活力 | 454.09% |

| 融通健康产业 | 172.66% | 交银定期支付双息平衡 | 151.56% | 易方达中小盘 | 448.20% |

根据数据统计,A股市场近十年涨幅74.4%,而基金近十年涨幅145.18%。

According to WIND statistics, the A-share market has risen by 74.4% in the past ten years, while funds have risen by 145.18% in the past ten years.

三,国内公募基金表现(偏债)

Wind数据,今年上半年债券基金表现

3. Performance of domestic public offering funds (debt inclined)

Wind data, bond fund performance in the first half of this year

| 固收+/ Fixed income+ | 债券型Bond | 可转债Convertible Bond | |||

| 同类平均 Peer Avg. | 3.48% | 同类平均 | 2.01% | ||

| 招商睿祥 | 17.52% | 鹏华可转债 | 14.59% | 鹏华可转债 | 14.59% |

| 泓德致远 | 17.04% | 华夏鼎利 | 12.93% | 宝盈融源可转债 | 11.24% |

| 易方达安盈 | 14.97% | 光大添益 | 12.27% | 申万菱信 | 8.05% |

| 鹏华可转债 | 14.59% | 宝盈融源可转债 | 11.24% | 中银转债 | 8.01% |

| 鹏扬景欣 | 14.42% | 富安达增强收益 | 10.42% | 汇添富可转债 | 7.31% |

随着国内理财开始打破“刚性兑付”,货币政策宽松,银行,信托,券商,基金公司的“固收”产品都在趋向结构化,净值化管理,债券型产品陆续做为中长期的稳健配置,其中可转债由于具有转股预期,受益于股市的影响,今年以来走出较好收益,继续看好可转债基金配置。

As domestic financial management began to break the “rigid redemption” and monetary policy was loose, the “fixed income” products of banks, trusts, brokerages, and fund companies are all tending to become in structure and net worth management, and bond products are gradually being used as a medium and long-term stable configuration.

Among them, convertible bonds are expected to be converted into shares and benefited from the impact of the stock market. Since the beginning of this year, they have achieved better returns and continue to be optimistic about the allocation of convertible bonds.

That Northbound WM n AM opportunities.

Southbound will be HKMA/SFC accredited ELI, DCI, FX structured products, Accredited mutual funds n Fund Linked Elis….

Pls take a look at the above as I have recently made various presentations on RMB as replacement investment ccy underlying for both USD n HKD.😎👍

Launch of the Cross-boundary Wealth Management Connect Scheme in the Greater Bay Area – KPMG

Outline Development Plan of the Central Government and the State Council for the Guangdong-Hong Kong-Macao Greater Bay Area (Outline Development Plan) in February 2019, and the Opinions Concerning Financial Support for the Establishment of the Guangdong-Hong Kong- Macao Greater Bay Area

1) Promote investment diversification and facilitate the flow of capital in the GBA; and

2) Promote RMB internationalisation and strengthen Hong Kong’s status as an international financial centre and offshore RMB hub.

……….The growing wealth of mainland Chinese residents is leading to increasing demand for investment diversification to offshore assets. At the same time, increasingly active northbound trading through Stock Connect and Bond Connect indicates that investors in Hong Kong are interested in mainland China’s capital markets and in increasing their exposure to mainland China-related investments. FTSE Russell’s inclusion of A-shares and MSCI’s increased weighting of A-shares in their respective indices are expected to further boost northbound trading.

…………….In August 2019, the stock exchanges in Hong Kong, Shanghai and Shenzhen agreed on the criteria for including Hong Kong-listed stocks with weighted voting rights in the Stock Connect schemes. Following this agreement, in October 2019, the first batch of eligible stocks with weighted voting rights was included in southbound trading for Stock Connect, and trading volumes have since increased.

…………The scheme has a southbound and a northbound component, depending on the residency of the investors. Under the Southbound component, residents of the mainland Chinese cities in the GBA will be able to invest in eligible WMPs distributed by banks in Hong Kong and Macao by opening designated investment accounts with those banks. Under the Northbound component, Hong Kong and Macao residents will be able to invest in eligible WMPs distributed by mainland Chinese banks in the GBA.

As of now, there are six foreign-funded legal person banks (HSBC; SCB; HS; BEA; DBS; Citi) (solely foreign-funded banks, equity joint banks, solely foreign-funded financial companies and equity joint financial companies) in the GBA. In February 2020, one year after the issuance of the Outline Development Plan, foreign banks from 13 countries and regions have established a total of 155 business institutions in Guangdong province (excluding Shenzhen), making Guangdong the first province to have foreign banks in all prefecture- level cities.

……………..Wealth Management Connect represents another significant development in the liberalisation of mainland China’s capital account following the launch of QFII/QDII, the Mainland-Hong Kong Mutual Recognition of Funds scheme, and the Stock Connect and Bond Connect schemes.

Under Wealth Management Connect, cross-boundary remittance will be carried out in RMB, with currency conversion conducted in the offshore markets. Cross-boundary remittance will also be conducted and managed in a closed-loop through the bundling of designated remittance and investment accounts (Type 1 Account). Through this mechanism, residents of the mainland Chinese cities in the GBA can directly use RMB to invest in eligible investment products distributed by banks in Hong Kong and Macao, and residents in Hong Kong and Macao can use offshore RMB to invest in eligible RMB-denominated assets distributed by mainland Chinese banks in the GBA. Cross-boundary fund flows will be subject to aggregate and individual investor quota management.

These developments will accelerate RMB internationalisation and strengthen Hong Kong’s position as a global offshore RMB hub.

………………….investors with greater product diversity and asset allocation options, while also raising the bar for financial institutions in terms of product design, service quality and risk management. Wealth Management Connect will be governed by the respective laws and regulations on retail wealth management products applicable in mainland China, Hong Kong and Macao. To this end, the regulatory authorities will introduce measures and establish robust mechanisms for regulatory cooperation, communication and coordination in order to protect the interests of investors. In addition, a long-term mechanism for financial risk management needs to be established to address issues in areas such as compliance, liquidity and cross-boundary risks. Specific policies and measures should be implemented on a pilot basis and enhanced gradually.

In our view, there are a number of key areas that financial institutions should focus on:

Their relevant products’ risk management, compliance and operation processes must meet the regulatory requirements in all three regions prior to cross-boundary distribution.

The design of the WMPs must consider the risk tolerance of investors and whether they are qualified investors. Conduct and sales suitability should be high on the agenda to avoid instances of misleading sales practices or the mis-selling of WMPs.

Before selling WMPs, sales agencies must clearly explain to investors the risk management measures, relevant laws and regulations, and relevant provisions for the protection of investors’ rights and interests for WMPs in the different regions in the GBA.

Financial institutions should also establish and improve their risk management systems to enhance the timeliness and efficiency of risk alerts and reduce their risk levels. Wealth Management Connect will also place greater demands on the comprehensive wealth management capabilities of banks in areas such as sales channels, customer service, product management, risk management and information disclosures.

Conclusions

………………………Wealth Management Connect is expected to drive greater product innovation, and may attract more international financial institutions to set up or expand their presence in Hong Kong and the other GBA cities to capitalise on these opportunities and tap into a large investor base. This will likely spur more competition in the region, which should raise the bar for product diversity and quality, and robust risk management.

Following the launch of the Stock Connect and Bond Connect schemes, Wealth Management Connect stands as another example of deepening financial cooperation between mainland China, Hong Kong and Macao. It also presents new growth opportunities for the region’s banking and asset management industries, cements Hong Kong’s status as an international financial centre and offshore RMB hub, and reinforces the GBA’s leading role in China’s economic growth and opening up.

APPENDIX

Option trading with underlying assets

Instead of maintaining naked positions, investors can combine a simple option strategy with positions in the underlying asset to modify the portfolio payoff. Some of these modified strategies can also serve a hedging purpose.

Covered Calls

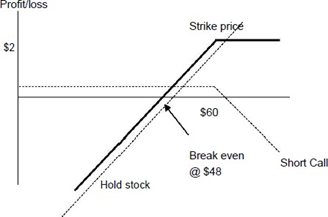

A covered call strategy involves selling a call option against a stock position already held. An investor pursuing this strategy will receive the option premium immediately by selling the call. However, there is a trade-off. In case stock price rises, the investor is obliged to give up his stock at the strike price under the option contract. As the strike price is lower than the spot price (otherwise the option buyer will not exercise the option), the covered call investor will lose the opportunity to benefit from the capital appreciation in the stock.

As an example, assume that an investor holds 100 shares of stock where currently the price is $50. The investor sells 100 call options on the stock with a strike price of $60, collecting a premium of $2 per share.

Upon expiry of the option,

- if the stock price is below $60, the option would expire worthless and there is a total gain of $200 ($2 x 100) from the options, which is the option premium received earlier. The breakeven price is $48 ($50 – $2).

- if the stock price is above $60, the 100 shares will be “called away” and investor is obliged to sell the 100 shares to the option holder at the strike price of $60. He still earns the $200 premium already received, however, he has lost the capital appreciation from the stock (from the $60 point onwards).

Notice the diagram above is similar to the payoff for selling a naked put.

Writing covered call options has been a popular investment strategy among institutional

investors. An equity fund manager may find it appealing to write calls on some of the stock in the fund. Although they will forfeit the potential capital gains should the stock price rise above the strike price, they are able to boost the fund performance by the premiums collected if they plan to sell the stock at the strike price anyway.

In this manner, a covered call has some resemblance to placing a limit sell order on a stock currently held, at a higher price than the market price: the investor is seeking to dispose of the investment but hopefully at a better price. There are two important differences:

One gets paid for a covered call.

A covered call is a contract. Unlike a simple sell order that can be cancelled anytime, it is not so easy to back out of a written call, without incurring some unwind costs.

Protective put

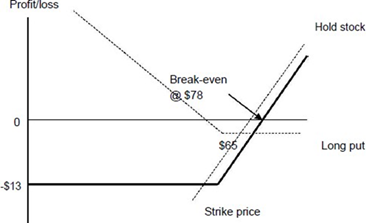

Suppose you would like to invest in a stock, but you find it too risky as you are hesitant to bear potential losses beyond a given level. In this case, you might consider a protective put strategy in which you invest in the stock while purchasing a put option on the stock simultaneously.

Consider a portfolio consisting of one share of stock (selling at $75) and one put option on that share (option premium = $3) with a strike price of $65. On the expiration date of the option,

- if the stock price is above $65, the put option will expire worthless. The portfolio value is equal to the stock price. The breakeven point is $78 ($75 + $3).

- if the stock price is below $65, you will exercise the put option and sell your share at $65. Therefore, the portfolio value is secured at $65.

Simply stated, the put option provides a kind of portfolio insurance. If the stock price rises, the portfolio value will rise right along with it. If it falls, the put option guarantees that the stock can be sold for a certain amount. The following shows the payoff diagram of a protective put strategy.

Notice the diagram above is similar to the payoff for buying a call.