HKSFC Licensed Corp #ADC118

September Newsletter

L & C

August 23, 2019

October Newsletter

September 27, 2019September Newsletter

Market Analysis

Equity Markets

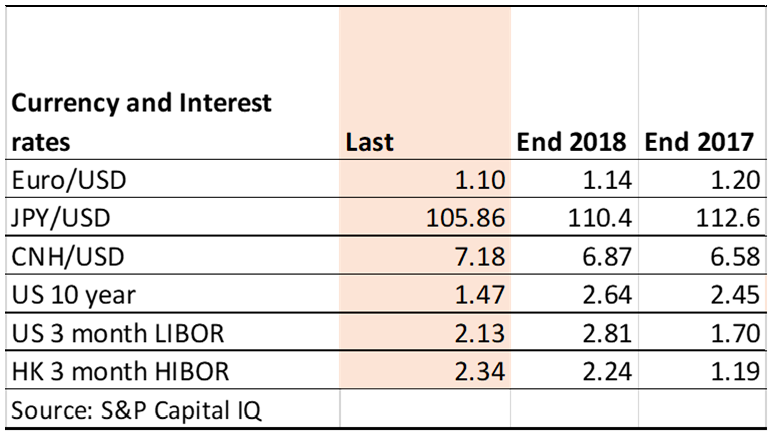

Since we last wrote on August 15, Global equity markets have rallied by around 2.3%. No region has notably outperformed or underperformed. As of September 1, a new fifteen per cent tariff was imposed by the US on USD112bn of exports from China. In response, Beijing said it would raise existing tariffs on US$75 billion worth of US goods by between 5 and 10 per cent, in two steps, on September 1 and again on December 15, in line with the US schedule. Despite that the MSCI China index rallied by 3.0% over the period encouraged by the ongoing trade talks between the US and China. A further boost for equity markets is the extremely low interest rates with the US 10-year treasury at 1.5%. The 12-month trailing yield on the S&P 500 ETF is 1.99%, so unless one thinks that the S&P 500 companies are going to cut their dividends an investment in the US stock market is more attractive than US government bonds. Amongst sectors those with high dividend yields such as Utilities and Real estate have outperformed, Health Care has underperformed due to concerns that the sector’s pricing power is diminishing, Energy and Materials have also underperformed due to concerns on the strength of the economy.

Fixed Income and FX markets

Over the past two weeks US interest rates have continued to weaken slightly. The RMB and the Euro have also weakened due to poorer economic outlook in those areas. It’s curious that there has been a big rally in both the Fixed Income and Equity this year, but it’s probably explained by the very loose monetary policy globally. Once this tightens, we expect a selloff in the Government and Investment Grade bond markets. However, as higher interest rates are likely to coincide with more optimism on the global economy, Global Equity markets should fare better once the interest rate cycle reaches a bottom.

Global Stock Model Portfolio

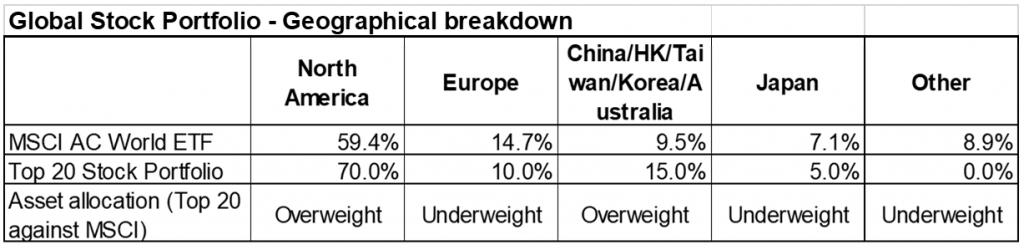

Due to relative price movement between Cisco and Intel we have decided to sell Cisco from the Global stock portfolio and replace it with Intel, which now has a larger weight in the MSCI Index than Cisco . The country and sector weights remain unchanged – refer to the following tables. An updated stock list is sent as an appendix to this note. As of September 3, 2019, the portfolio has returned 1.42% compared with a 1.95% return for the MSCI AC Index

Global ETF portfolio

Since its inception on August 2 the Global ETF portfolio is down by 0.7% compared with a 1.1% decline in the MSCI AC World Index. We are waiting for a market correction before investing the remaining 10% of the portfolio. The decision to be overweight the US, China and Cash has helped the portfolio, whereas the overweight in Communication Services has detracted.

Fixed Income Bond and ETF portfolio

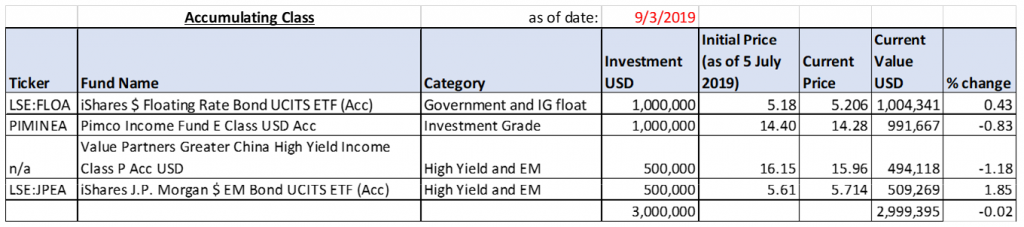

The fixed Income Bond and ETF portfolio has suffered by being a short duration. Therefore, it has not gained that much benefit from the collapse in long bond yields. That together with some widening in Chinese credit spreads has led to declines in value for the Pimco Income Fund and the Value Partners Greater China HY fund. This was partly made up for by the JP Morgan EM Bond fund, which has a duration of 7.7 years, the iShare Floating rate bond fund gave stable returns as expected. With the US 10-year treasury at 1.5% we think that further declines are unlikely – so we chose not to change the Fixed Income strategy.

All the information contained in this document is as of date indicated unless otherwise noted.

This document is issued by Axiom Investment Management Limited and has not been reviewed by the SFC. It may not be reproduced, distributed or transmitted to any person without express prior permission. This document and the information contained herein may not be distributed and published in jurisdictions in which such distribution and publication is not permitted.

Nothing contained here constitutes investment advice or should be relied on as such. The value of securities mentioned in the report and the income from it, if any, may fall or rise. Past performance of the securities mentioned in the report is not necessarily indicative of its future performance.

Axiom Investment Management Limited, 25/F, 168 Queen’s Road Central, Hong Kong. Telephone: 852 2537 2030 Facsimile: 852 2868-0091. Web: www.axiom-invest.com