HKSFC Licensed Corp #ADC118

2021 1H MARKET UPDATE

Institutional Asset Management business model & development – Janet Li from Mercer @ HKU

June 4, 2021

2021 1H Global Asset Allocation Portfolio Review

July 5, 20212021 1H MARKET UPDATE

MARKET UPDATE

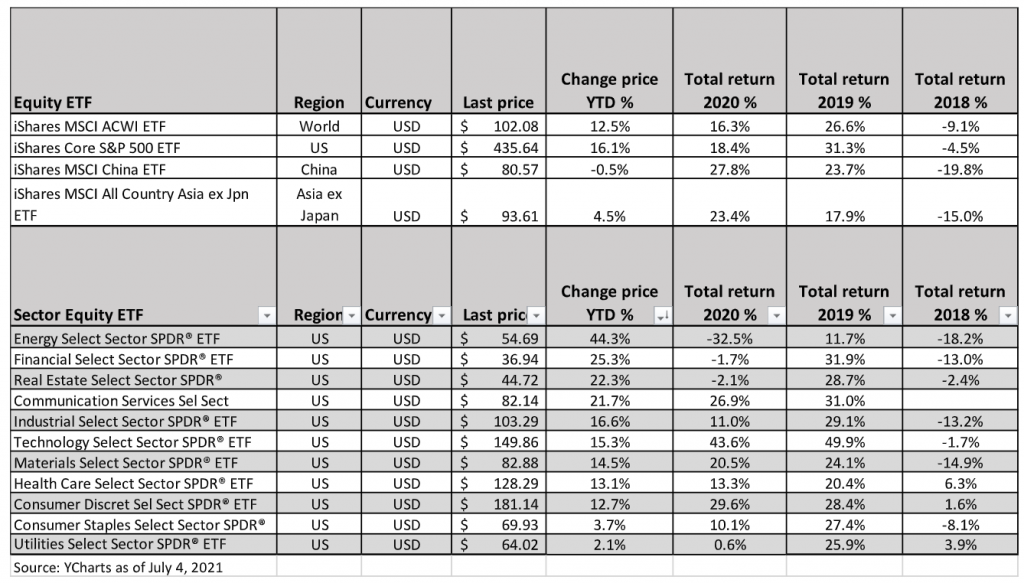

Equity market performance by region and sector 2021

Global Equity markets have made steady progress in 2021. The US is the relative outperformer with the S&P500 increasing by 16.1% so far this year, whereas the MSCI AC World index has increased by 12.5%. MSCI China has been the laggard declining by 0.5%. That is because the Chinese Equity market has been held back by the tough stance of the Chinese regulators against Alibaba, Ant Financial Tencent, Meituan and other major Internet companies.

By sector, the top performers in the US were: Energy (travel resuming), Financials (improved economy) and Real Estate (improved economy together with low interest rates). The worst performers were Utilities and Consumer Staples as investors preferred more cyclical sectors.

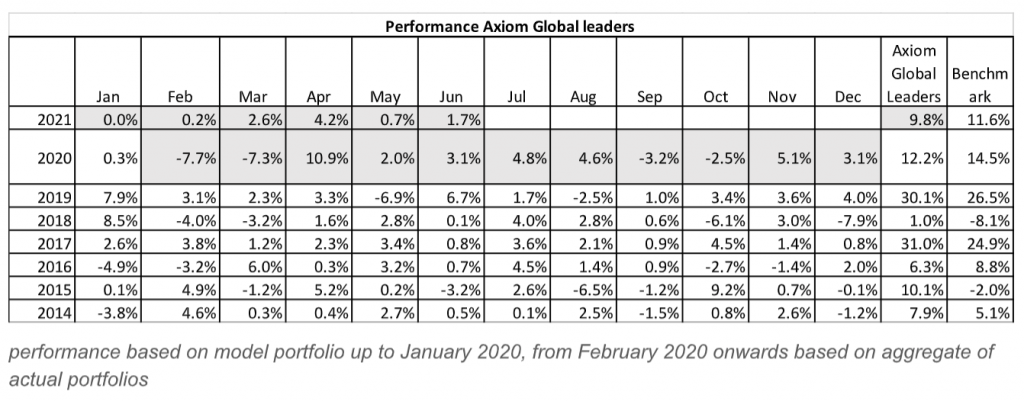

AXIOM GLOBAL SECTOR LEADERS PORTFOLIO REVIEW

In H1 2021 the portfolio has increased by 9.8% vs a 11.6% gain in our benchmark, the iShares MSCI ACWI ETF. The top contributor the performance were holdings in: Alphabet, Facebook, and Microsoft. The top three detractors were: Alibaba, P&G and not owning Energy Stocks

We have made the following changes to the portfolio

Sold Merck and purchased iShare on Global Clean Energy. We sold Merck as the company stock price underperformed leading it to no longer qualify as a Global Sector Leader. The underperformance is partly due to the forthcoming end to the exclusivity period of its diabetes medicine, Januvia.

We purchased the iShare on Global Clean Energy (ICLN). It should benefit as the world moves away from fossil fuels to Wind, Solar, Hydrogen and other Clean energy sources. Share price had corrected before our purchase bringing valuations to more reasonable levels

MARKET OUTLOOK

We believe there is room for meaningful upside in global equities in 2021 although it has already risen 12.5% so far this year

There are three main reasons for this, in our view 1) a successful COVID-19 vaccine that leads to a return to economic and corporate profits growth; 2) a reduction in the equity risk premium driven by lower uncertainty and volatility; and 3) sizeable inflows into equity funds as the large amount of cash remaining on the sidelines re-enters the market

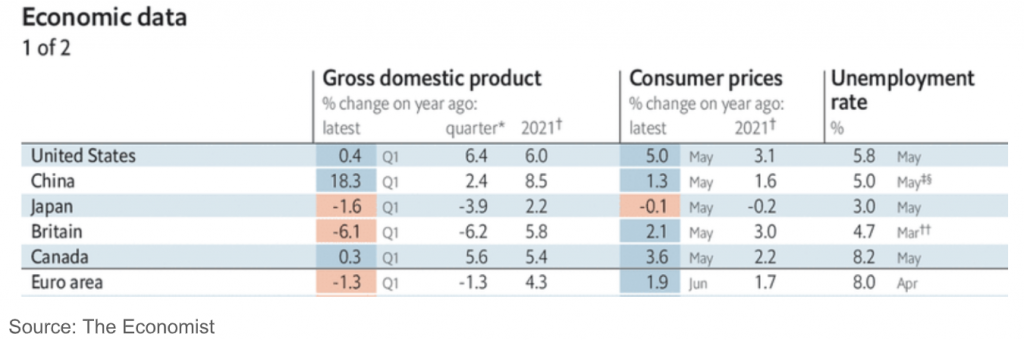

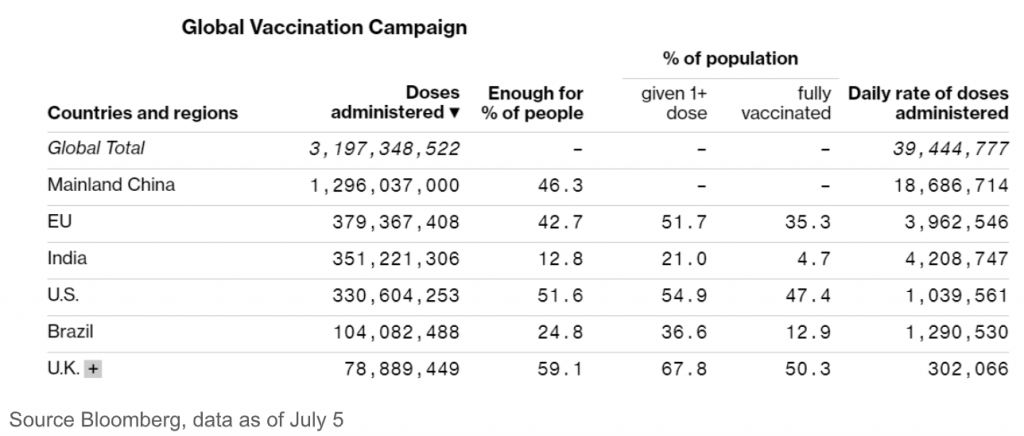

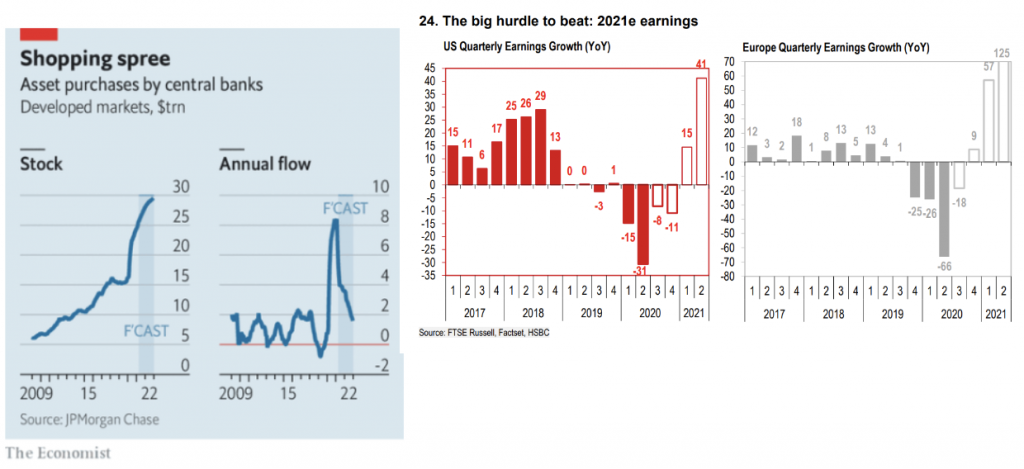

As we look ahead to the second half of 2021, the global recovery from the pandemic remains resilient despite new risks to the outlook. We expect the world economy will expand by more than 6.0% this year, led by economies that have successfully kept the virus under control (China) or who have quickly vaccinated significant shares of their populations (the US and the UK). Growth in the Euro area may lag but the recent pick up in vaccination rate in the Euro area should lessen the impact of Covid variants.

Mainland China and the US and EU, being the world’s major economies have high vaccination rates at over 40% of their populations. Based on the present daily vaccination rates these coverage rates should go up significantly by the end of 2021. The successful rollout of vaccines should lead to strong Q2 earnings from companies in the US and Europe

The other main threat comes from higher US inflation rates over the summer. The Federal Reserve’s target measure of inflation – changes in personal consumption expenditure prices –is now running well above its 2% goal. The Fed, however, expects summer increases in inflation above its 2% target will only be temporary. Elevated price increases are due to pent-up demand and supply chain lags. The comparison to last year’s weak levels — at a time when the economy was mostly shut down — is also a factor. We concur with this view and think that increased use of Technology by major companies will be effective in keeping inflation under control over the medium term.

If the Fed is right and core inflation peaks over summer at around 3% before falling back towards its 2% target, then risk assets will remain supported as Central Banks will continue to make bond purchases well into 2022. Further, the Fed will be able to keep its policy rates near zero until 2022 to continue supporting the economy’s recovery from the pandemic

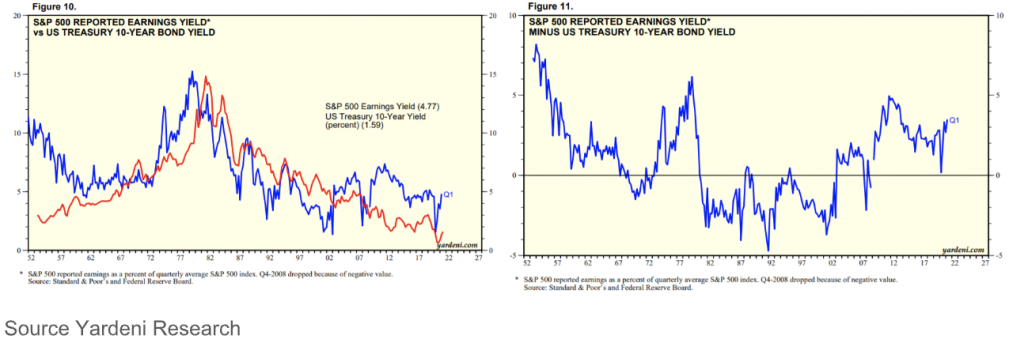

The forward PER of the US market is 21.0X meaning the forward earnings yield is 100/21 or 4.77%. The gap between the S&P forward earnings yield and 10-year US Treasury yield is 3.18% which is referred to the Earnings Risk Premium (ERP). This is high relative to the long-term historical pattern (see chart on next page).

We think that the PER of the US market can move to 25 (Earnings yield 4%) and it would remain at a reasonable 2.4% premium to the US treasury Yield. A PER of 25 would mean that US market still has another 15% upside in 2021

All the information contained in this document is as of date indicated unless otherwise noted.

This document is issued by Axiom Investment Management Limited and has not been reviewed by the SFC. It may not be reproduced, distributed or transmitted to any person without express prior permission. This document and the information contained herein may not be distributed and published in jurisdictions in which such distribution and publication is not permitted.

Nothing contained here constitutes investment advice or should be relied on as such. The value of securities mentioned in the report and the income from it, if any, may fall or rise. Past performance of the securities mentioned in the report is not necessarily indicative of its future performance.

Axiom Investment Management Limited, 25/F, 168 Queen’s Road Central, Hong Kong. Telephone: 852 2537 2030 Facsimile: 852 2868-0091. Web: www.axiom-invest.com