HKSFC Licensed Corp #ADC118

April Newsletter

March Newsletter

February 19, 2020

Webinar With Seasoned Banker, Alvin Ma

May 5, 2020April Newsletter

MARKET UPDATE

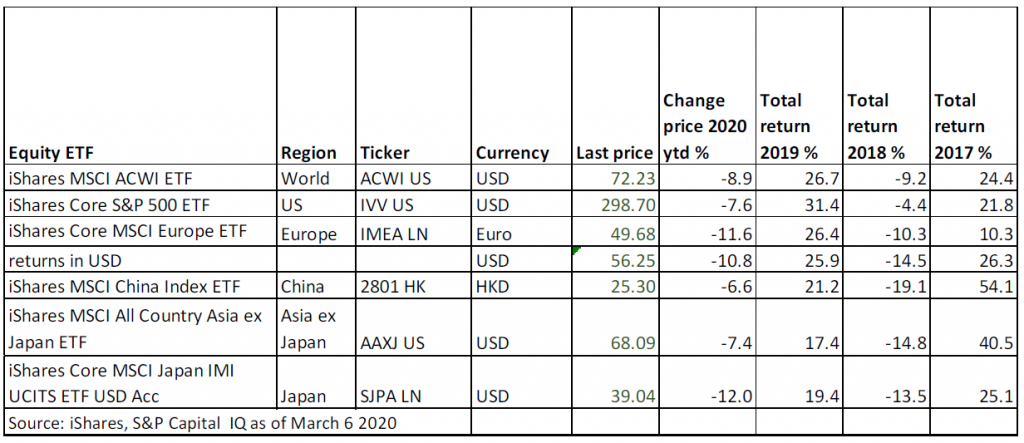

Equity market performance by region 2020

After initially reacting calmly to the outbreak of the Covid 19, the rapid spread from China to the rest of the World of the virus has rocked global financial markets so far this year. The MSCI AC World Index is down 8.9% year to date. There are currently 110,110 confirmed cases and 3,831 deaths from the coronavirus COVID-19 outbreak as of March 09, 2020, 08:00 GMT.

Financial markets believe that China has Covid 19 under control and that the authorities will implement aggressive stimulus measures. This has led MSCI China to be the outperformer so far this year being only down 6.6%. The US market is also an outperformer with the S&P 500 Index down by 7.6%. The US has been helped by two factors being

1) The U.S. Federal Reserve cut interest rates by 50 bps on Tuesday March 3 in a bid to shield the world’s largest economy from the impact of the coronavirus. It was the first rate cut outside of a regularly scheduled policymaker meeting since 2008 at the height of the financial crisis.

2) The comeback of Joe Biden at the Super Tuesday primaries leading to a big bounce in the US health care sector. Biden’s delegate wins lessen the chance that Medicare for All, which would virtually eliminate the private health insurance sector, would become a reality. That being the policy favored by his rival Bernie Sanders.

Europe and Japan are the laggard markets due to the rapid spread of Covid 19 in Europe and the lack of strong policy responses to the impact of Covid 19 to their economies.

Have the markets reached a bottom yet?

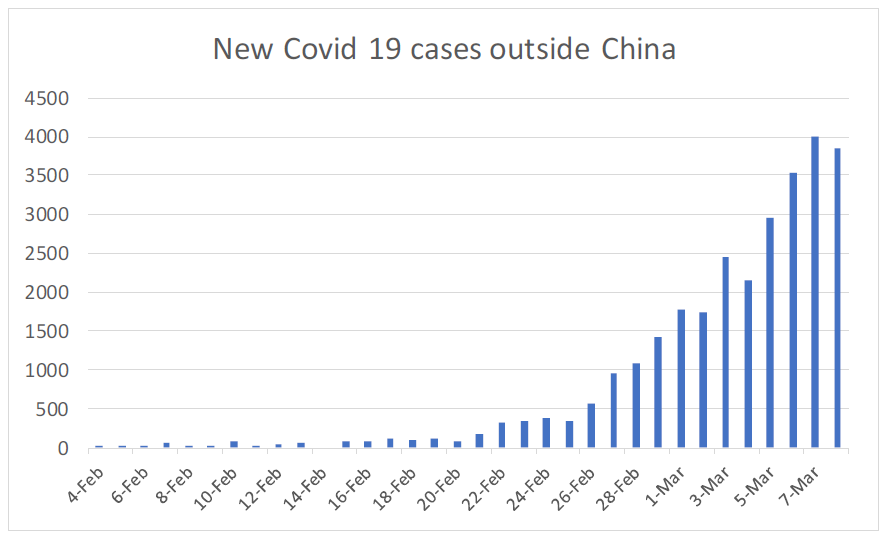

Covid 19 infections in China peaked at around 3,800 cases per day on Feb 4, 2020 ( excluding the reclassification that took place on Feb 12, 2020) and that coincided with a rally in MSCI China ETF, which continued until Global cases started a worrying build up towards the end of February

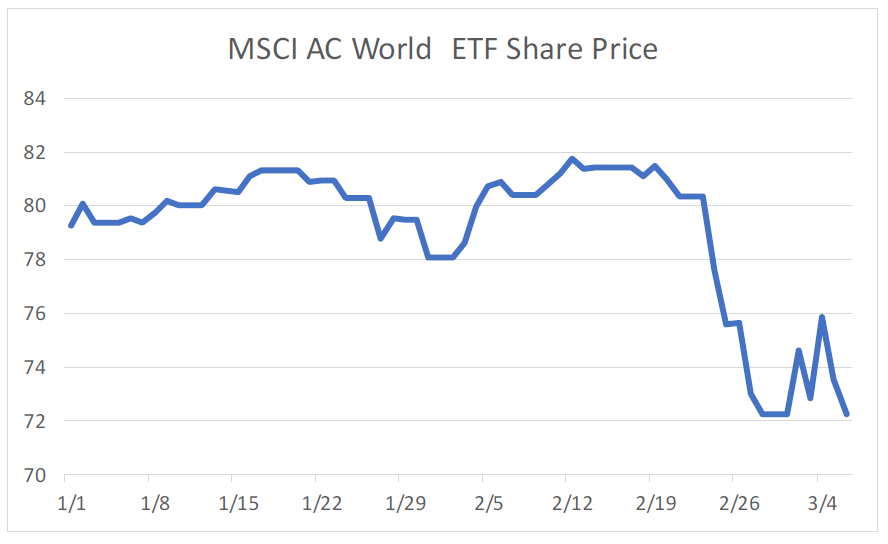

Looking at the performance of the MSCI AC World ETF, we can see that Covid 19 has also been a driver. The big fall in the global markets took place from February 23, around about the time that cases outside China started to accelerate. Global markets are still very volatile and have yet to find a bottom with the following factors influencing the markets:

1) New Covid -19 cases have not peaked yet even though it appears to have stabilized in recent days

2) US fed has cut interests by 50 bps – see comments above

3) the policy response in the hot spots of Italy, Iran and South Korea show that these countries are willing to apply the lessons learnt in China leading to optimism

4) Oil prices drop sharply as Russia increases supply

LESSONS LEARNT FROM PREVIOUS HEALTH CRISIES

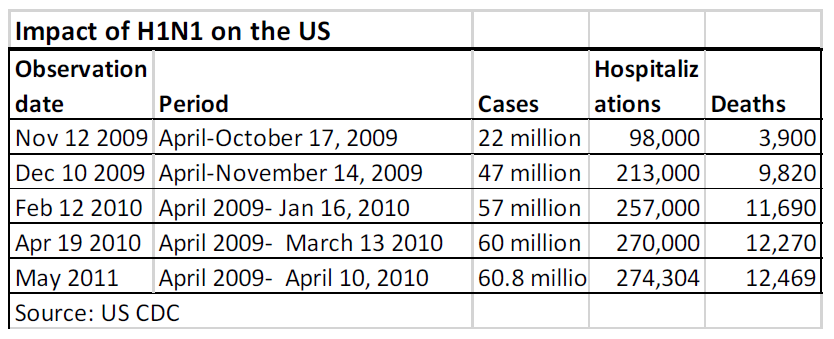

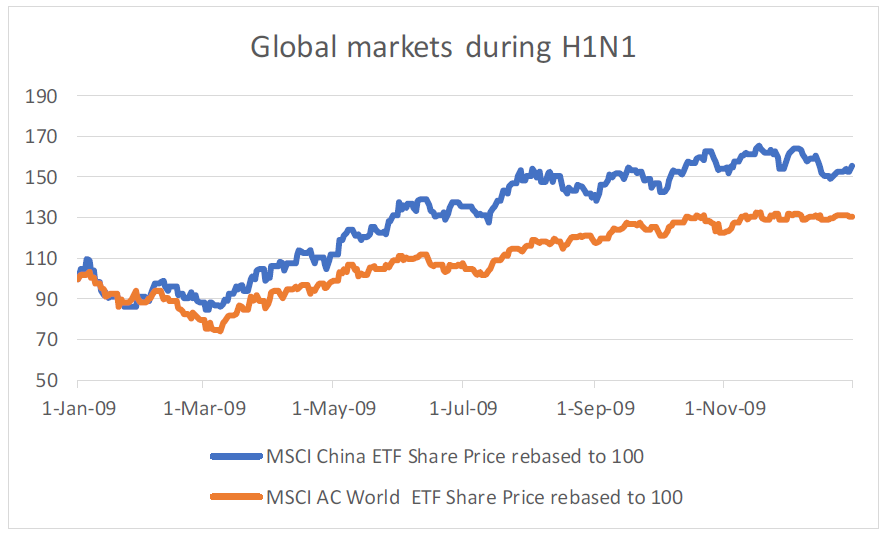

In the spring of 2009, a novel influenza A (H1N1) virus emerged. It was detected first in the United States and spread quickly across the United States and the world. This new H1N1 virus contained a unique combination of influenza genes not previously identified in animals or people. From April 12, 2009 to April 10, 2010, CDC estimated there were 60.8 million ases, 274,304 hospitalizations and 12,469 deaths in the United States due to the virus. While a vaccine was produced, it was not available in large quantities until late November—after the peak of illness during the second wave had come and gone in the United States. It should be noted that the CDC had revised up its estimates of the impact of H1N1 several times over the course of the illness.

Despite the large number of cases and deaths in the US caused by H1N1 in the US it did not have a significant impact on global equity markets. This may be because the markets were already at low levels and recovering from the impact of the Global Financial Crisis

Equity markets during SARS 2003

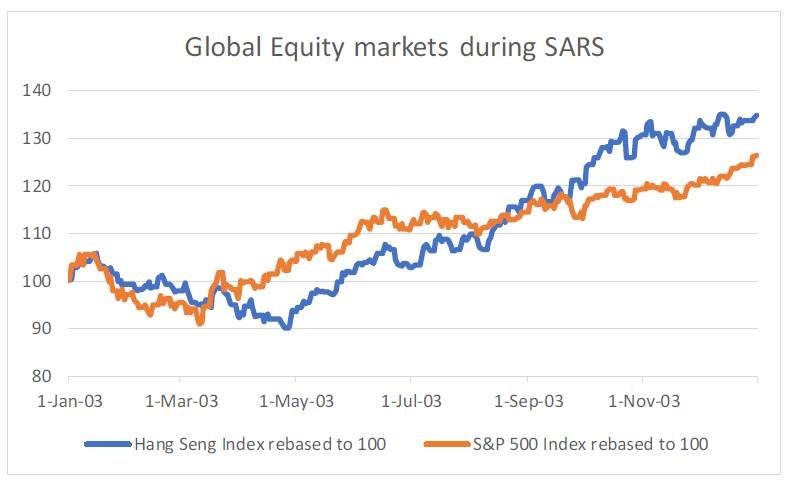

Hong Kong markets reached a bottom between 13-17 May 2003 during the SARS health crisis. This coincided with signs that SARS was being controlled. On 13 May the WHO reported “Outbreaks at the remaining initial sites show signs of coming under control, indicating that SARS can be contained”. On 23 May the WHO removed Travel recommendations for Hong Kong and Guangdong Province. US markets were less impacted by SARS reaching a bottom on March 10-12, when the SARS illness was still raging. However, this could be due to fact that US markets were just emerging from a bear market in 2003 and SARS was a less infections disease than COVID 19. However, its worth noting that the Hang Seng Index recorded a gain of 34.9% in 2003 whereas the S&P 500 recorded a gain of 26.4%

AXIOM GLOBAL SECTORS LEADERS PORTFOLIO REVIEW

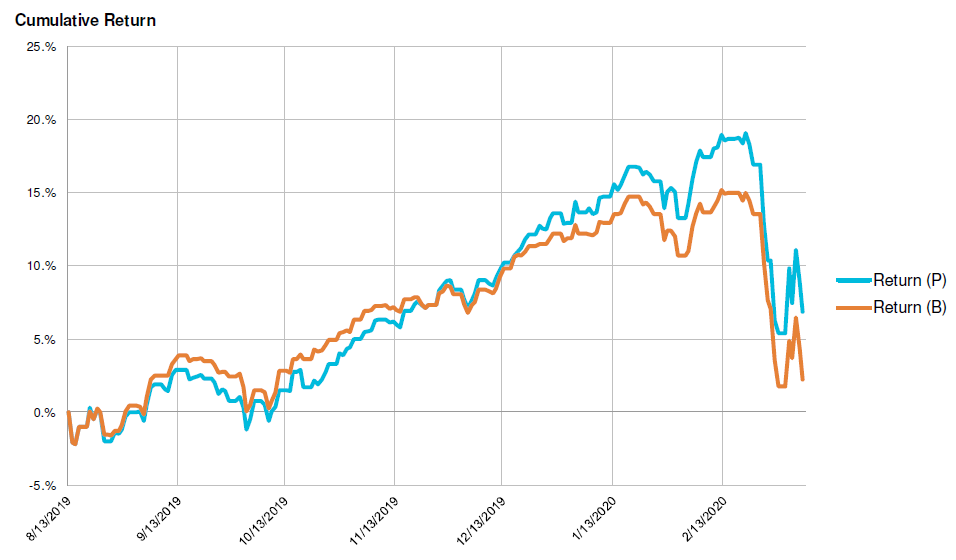

Chart of Portfolio performance vs the Benchmark from Inception on August 13 2019 to February 11 2020

The Global Seclor Leaders portfolio has returned 6.9% in the period Aug 13, 2019 to March 6, 2020 outperforming the benchmark return of 2.3%

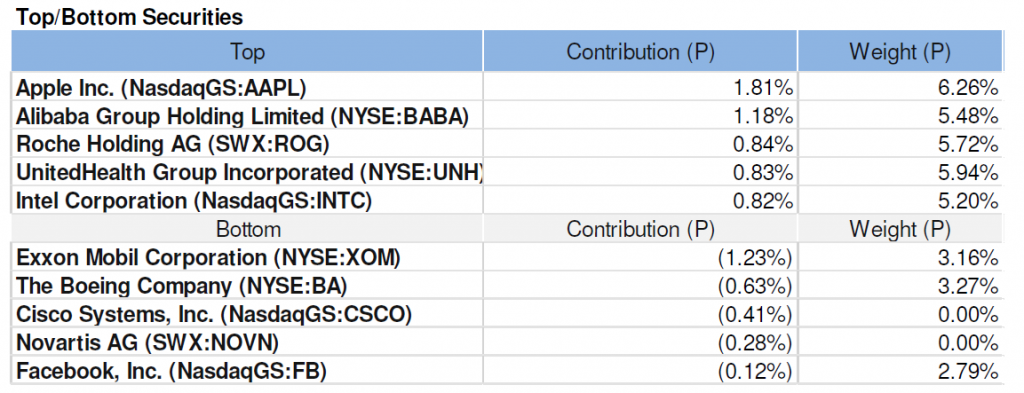

The top performing securities were the large Consumer Discretion, Health Care and Technology stocks. Of the Underperforming companies Cisco has been sold and replaced by Intel whereas Novartis was sold and replaced by Roche.

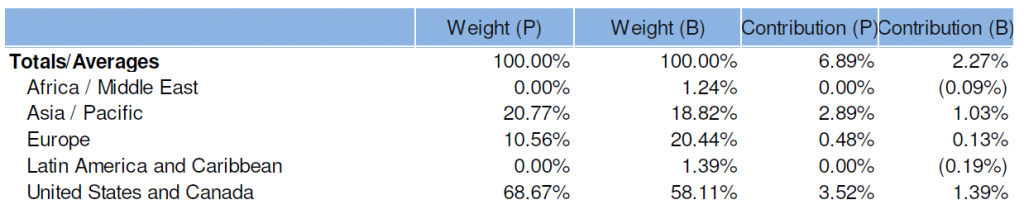

Global Seclor Leaders portfolio return by country

Analysing the returns by Country the majority of the returns have come from the United States followed by China ( within the Asia/Pacific region).

MARKET OUTLOOK

Going forward the market should stage a rebound once the number of new Covid-19 cases outside China has reached a peak – the experience in China and South Korea is that firm action by Public Health officials can achieve this within a reasonable space of time.

Philip Niem

All the information contained in this document is as of date indicated unless otherwise noted.

This document is issued by Axiom Investment Management Limited and has not been reviewed by the SFC. It may

not be reproduced, distributed or transmitted to any person without express prior permission. This document and

the information contained herein may not be distributed and published in jurisdictions in which such distribution and

publication is not permitted.

Nothing contained here constitutes investment advice or should be relied on as such. The value of securities

mentioned in the report and the income from it, if any, may fall or rise. Past performance of the securities mentioned

in the report is not necessarily indicative of its future performance.

Axiom Investment Management Limited, 25/F, 168 Queen’s Road Central, Hong Kong. Telephone: 852 2537 2030

Facsimile: 852 2868-0091. Web: www.axiom-invest.com