HKSFC Licensed Corp #ADC118

March Newsletter

Ms. Z

January 28, 2020

April Newsletter

March 10, 2020March Newsletter

MARKET UPDATE

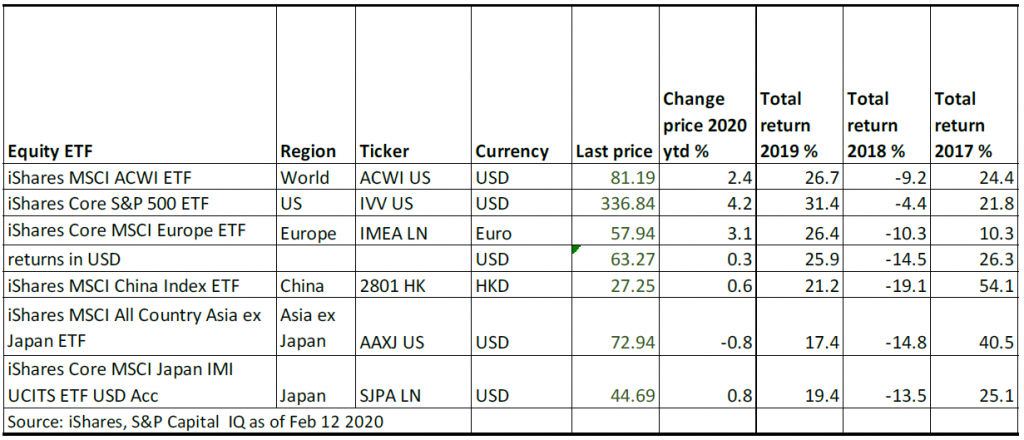

Equity market performance by region 2020

Global equity markets have rocked at the start of 2020 by several factors: firstly the US killing

Iranian commander Qassem Soleimani in a targeted airstrike and Iran retaliating by launching

a missile attack on two US military bases in Iraq secondly the outbreak of the Coronavirus

which could deal a blow to the global economy, threatening China related consumption and

tourism. It also disrupting global supply chains. Despite this Global equity markets are up by

2.4% so far in 2020, this has been led by the US which is up by 4.2%. Somewhat surprisingly

the MSCI China index is up by 0.6%. Europe and the rest of Asia are little changed in USD

terms.

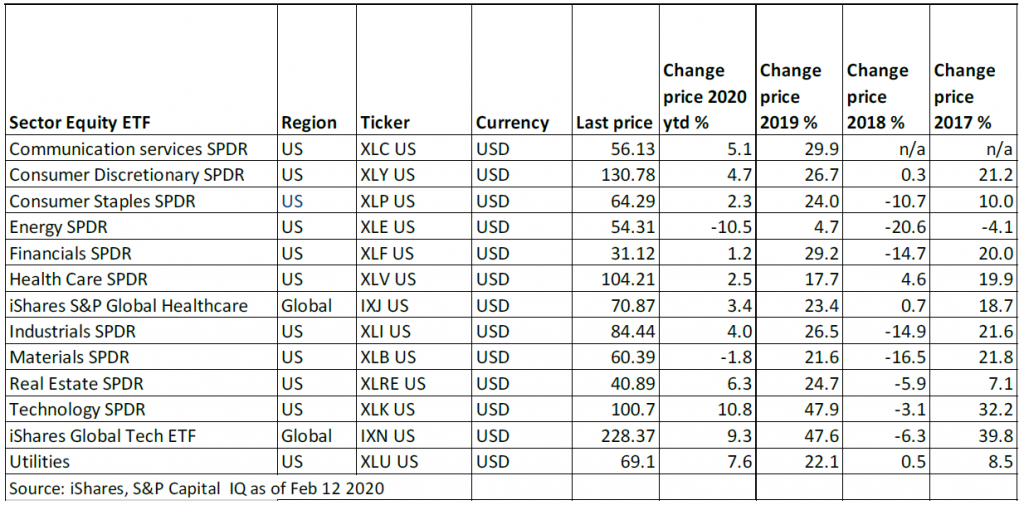

Equity market performance by sector 2020

By Sector Technology has delivered the best performance with the global sector up by 9.3%

and the US sector 10.8% for 2020 so far. This is due to well received earnings results. The

worst performing is the Energy sector as a slowdown in China is perceived to be negative for

oil prices. Equity markets have been helped by the decline in 10 year treasury yields from

1.91% end 2019 to 1.71% as of the time of writing. This has helped the Real estate and Utility

sectors in particular.

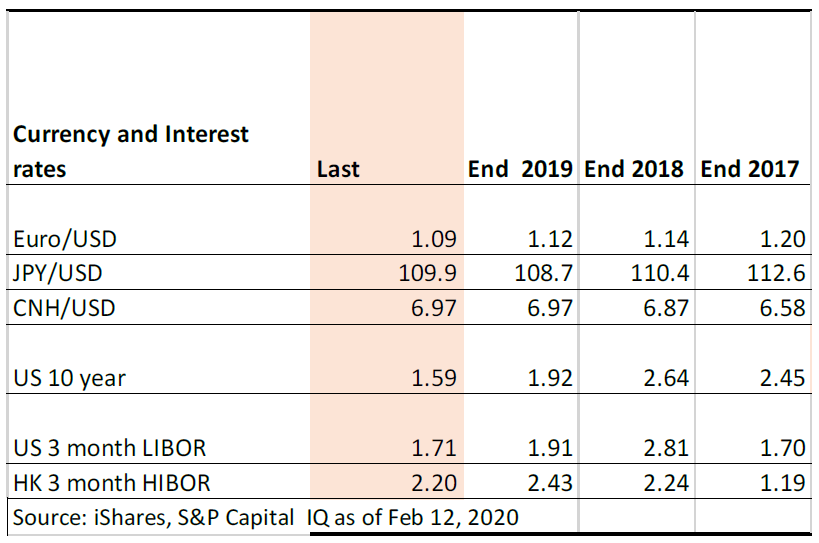

Currency and Interest rate snapshot

The potential negative impact of the Coronavirus on the Global economy has led to a decline

in US 10 year treasury yields from 1.91% end 2019 to 1.71% as of the time of writing. At the

same time pessimism on Europe’s economy and politics as caused a more than 2% decline in

the Euro vs the USD, whereas CNH is little changed as investors are optimistic that China’s

health care workers can contain the virus.

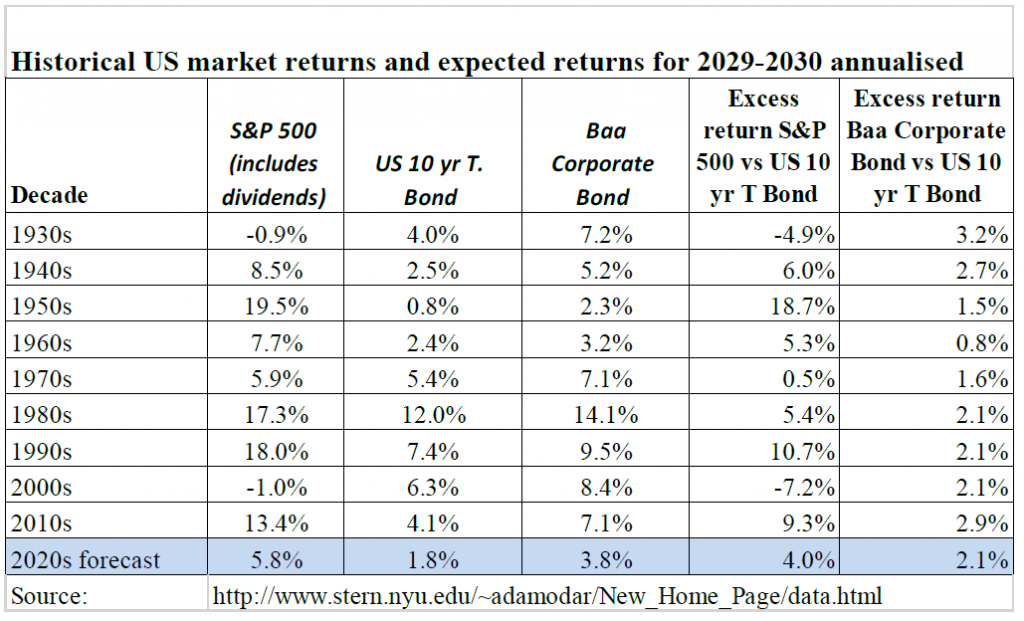

Market returns through the decades

The table below compares the returns of US equities and bonds by decade starting from 1930.

It shows that the only decades where the S&P 500 have recorded negative returns are the

1930s ( due to the great depression and second world war) and the 2000s ( due to the Tech

bubble bursting and the Global Financial Crisis). Those are only the only two decades where

the US 10 year Treasury returns beat thr S&P 500 returns

Our forecasts for returns over this decade?

The US 10 year Treasury yield started this decade at 1.9% but has since declined to 1.6% , we

think that a realistic assumption for average return of US 10 year Treasuries over the coming

decade is 1.8% p.a. Over the long term the S&P 500 total return has been 4.8% p.a higher that

that of US 10 Year Treasuries – using a more conservative 4% we predict that the S&P 500

total return will be 5.8% p.a over the next decade. Over the long term Baa rated corportae

bonds total return has been 2% p.a higher that that of US 10 Year Treasuries – using this we

predict that Baa corporate bonds total return will be 3.8% p.a over the next decade.

AXIOM GLOBAL SECTORS LEADERS PORTFOLIO REVIEW

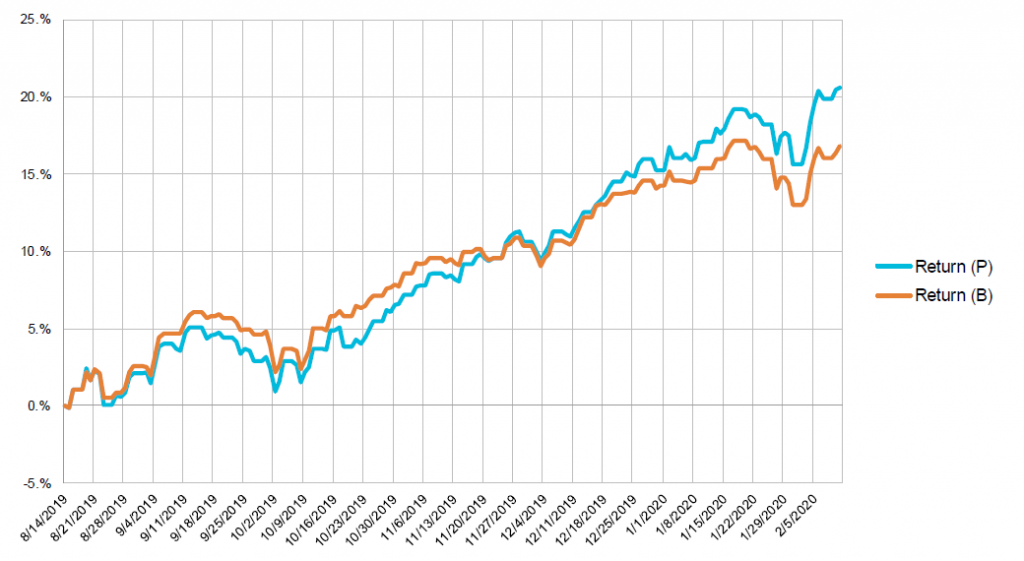

Chart of Portfolio performance vs the Benchmark from Inception on August 13 2019 to

February 11 2020

The Global Seclor Leaders portfolio has returned 20.57% outperforming the benchmark return

of 16.83%

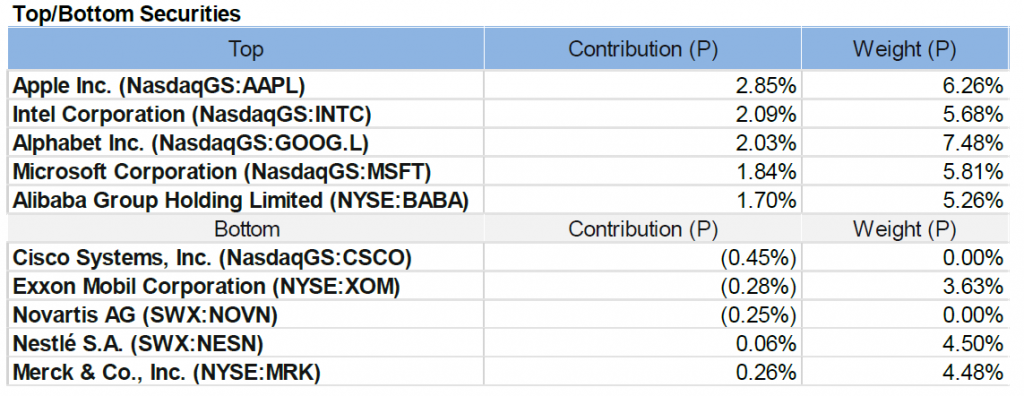

The top performing securities were the large Technology , Communications and Consumer

Discretion stocks in US and China. Of the Underperforming companies Cisco has been sold

and replaced by Intel whereas Novartis was sold and replaced by Roche.

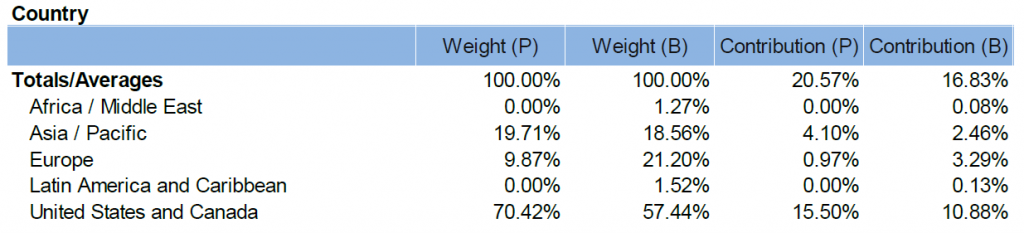

Global Sector Leaders portfolio return by country

Analysing the returns by Country the majority of the returns have come from the United States

followed by China ( within the Asia/Pacific region). Going forward the market may consolidate

at current levels for a while as the market assesses the impact of the Coronavirus on Q1

earnings. However, in the longer term we believe that our Global Sector Leaders equity

portfolio should outperform global equity markets – which should in turn outperform bond

markets and cash.

Philip Niem

All the information contained in this document is as of date indicated unless otherwise noted.

This document is issued by Axiom Investment Management Limited and has not been reviewed by the SFC. It may

not be reproduced, distributed or transmitted to any person without express prior permission. This document and

the information contained herein may not be distributed and published in jurisdictions in which such distribution and

publication is not permitted.

Nothing contained here constitutes investment advice or should be relied on as such. The value of securities

mentioned in the report and the income from it, if any, may fall or rise. Past performance of the securities mentioned

in the report is not necessarily indicative of its future performance.

Axiom Investment Management Limited, 25/F, 168 Queen’s Road Central, Hong Kong. Telephone: 852 2537 2030

Facsimile: 852 2868-0091. Web: www.axiom-invest.com