HKSFC Licensed Corp #ADC118

August Newsletter – Part II

August Newsletter – Part I

August 5, 2019

Mr. J

August 13, 2019August Newsletter – Part II

MARKET ANALYSIS

Equity Markets

After the sharp decline in markets on Monday August 5, following the decline of the RMB to

below 7 to the dollar – US markets have rebounded as the RMB has stabilized. They then

received a further boost as The US announced it would delay imposing tariffs on some imports

from China until 15 December because of “health, safety, national security and other factors”.

Since we last wrote on August 5, Global equity markets are down by around 0.4%. The US has

outperformed being flat, whereas the MSCI China market remains in the doldrums declining by

4.2%

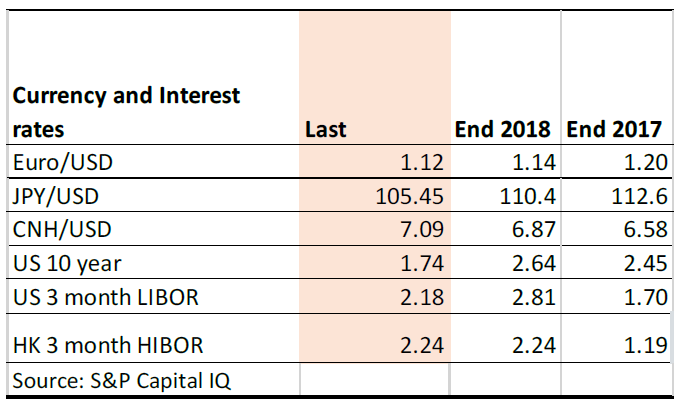

Fixed Income and FX markets

Over the past week US interest rates have continued to weaken and the market is now pricing

in that 3-month LIBOR will decline to close to 1% over the next years. Against that backdrop

the Euro has found some support at the 1.12 level and the Yen continues to strengthen.

Global Stock Model Portfolio

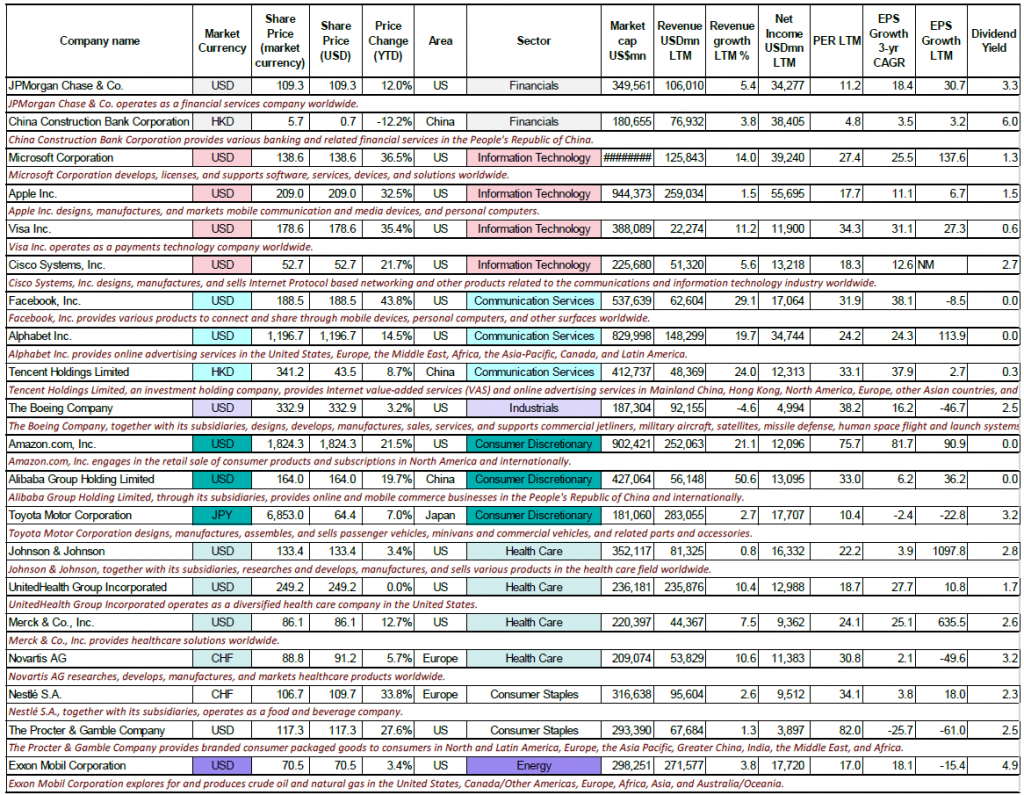

We have constructed a 20 stock Global stock portfolio which incorporates our Country and

Sector allocation decisions with the largest stocks in those sectors. The rationale for this is that

the largest stocks by market capitalization should be highest quality and most robust and

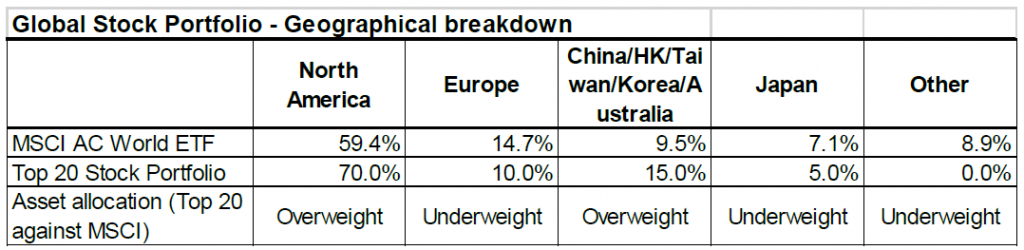

should therefore continue to grow over time. We allocate 10% to Europe (being underweight as we avoid the domestic banking sector which suffers from the political worries in Europe). The top two stocks in Europe by market capitalization are Nestle (the world’s largest consumer products including cosmetics company) and Novartis (one of the largest pharmaceutical companies by both market capitalization and sales. We have also decided to be underweight in Japan and consequently only own Toyota, which is the largest company by market capitalization there and the largest manufacturer of motor vehicles globally. In respect of China, we have selected the three largest stocks by market capitalization being: Tencent, Alibaba and China Construction bank. That is equivalent to a weight of 15% vs a neutral allocation to China and surrounding countries of 8.3%. Due to the relatively good value of MSCI China and that’s its capable of large rallies, I think that an equity portfolio for a China based investor should also be overweight in MSCI China.

The remaining 14 stocks are allocated to the US, which means that the portfolio is 70% invested in North America vs a neutral 59.4% – in line with our recommended asset allocation.

The stock selection in the US is based on our sector asset allocation. We are overweight Technology and recommend a 20% weight. New and improved technology drive business productivity and consumer spending so leading Tech companies should continue to be strong investments in our view. We then select the top 3 stocks by market cap in the sector which are: Microsoft, Apple and Visa. The fourth largest stock is Mastercard but as its business is similar to Visa, we decide against holding it in favor of Cisco, which is the world’s fifth largest Tech stock.

Our next largest weight is in health care, where we allocate 20%. This is an overweight position as i) historically the sector provides good downside protection in the equity market down turns) ii) it’s a sector where companies are continually making new discoveries to boost profits and iii) benefits from the ageing population. In addition to Novartis we hold the three largest health care stocks globally which are also based in the US being: Johnson and Johnson, United Health Group and Merck & Co.

We recommend a 15 % weight in the Communications sector, which is an overweight. We consider this sector has strong growth potential both in the US and globally as technology enables people to communicate more easily. The portfolio owns Tencent, which is the dominant company in China. In addition, in owns Alphabet and Facebook, which are the dominant companies outside of China. However, to recognize that Alphabet is a larger company we hold a weight of 7% in Alphabet and 3% in Facebook.

We also recommend a 15% weight in Consumer Discretionary, which is an overweight. We recommend Amazon which are the leading ecommerce companies in the US and the largest Consumer discretionary company globally. This combined with the position in Alibaba and Toyota, make up 15%.

We recommend a 10% position in Consumer Staples, which is slightly overweight. These companies have strong global brands so should be relatively defensive in an economic downturn. In addition to Nestle, the largest company globally, we also own US based Proctor and Gamble, which is the world’s second largest company in this sector.

We also own 10% in Financials, making it slightly underweight. Although financials generally outperform in a mild economic downturn, we don’t like it due to the high leverage in the business model. Furthermore, we don’t like European banks due to the exposure to political worries there. The model owns US based JP Morgan, the world’s largest financial stock in addition to China based China Construction Bank.

The portfolio owns 5% in Energy, which is a slight underweight. This is through US based Exxon Mobil, which is the worlds largest energy stock by market cap.

The portfolio also owns 5% in Industrials through Boeing, the worlds largest Industrial stock. We believe that the company will come through the crisis caused by the 737 crashes and keep its position as the worlds leading maker of commercial airplanes.

There is no ownership in the Materials, real estate or utilities sector as these are more localized businesses with no leading companies that are very substantial.

The portfolio is summarized in the table below. All the stocks have an initial portfolio weight of 5% with the exception of Alphabet with 7% and Facebook with 3%.

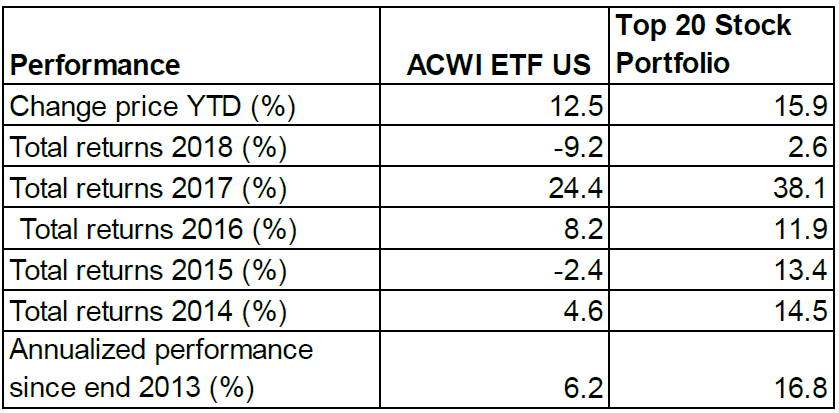

On a back test basis this portfolio has performed extremely well returning 16.8% p.a on a compound basis since the end of 2013 way outperforming the 6.2% p.a return of the MSCI AC World ETF and also outperforming the 8.7% p.a return of the Global ETF portfolio that we set up. However, this is flattering as by definition the to 20 stocks now have done well which is

why they have ended up being in this category. Going forward we will track the portfolio and

make a rebalancing in one of the two cases: i) a sector or country rebalance ii) one of the

stocks falls out of the top 20 and is replaced by another stock in which case we would remove

the stock from the model and replace it with the new one.

All the information contained in this document is as of date indicated unless otherwise noted.

This document is issued by Axiom Investment Management Limited and has not been reviewed by the SFC. It may

not be reproduced, distributed or transmitted to any person without express prior permission. This document and

the information contained herein may not be distributed and published in jurisdictions in which such distribution and

publication is not permitted.

Nothing contained here constitutes investment advice or should be relied on as such. The value of securities

mentioned in the report and the income from it, if any, may fall or rise. Past performance of the securities mentioned

in the report is not necessarily indicative of its future performance.

Axiom Investment Management Limited, 25/F, 168 Queen’s Road Central, Hong Kong. Telephone: 852 2537 2030

Facsimile: 852 2868-0091. Web: www.axiom-invest.com