HKSFC Licensed Corp #ADC118

August Newsletter – Part I

July Newsletter

July 5, 2019

August Newsletter – Part II

August 7, 2019August Newsletter – Part I

Equity Markets

Since we last wrote on July 5, Global equity markets have declined by 3.2% despite the 25 bps cut in the Fed funds rate. The surprise imposition of extra tariffs on PRC exports tweeted by US President Trump has unnerved markets. The US has been relatively defensive declining by 1.8%, whereas MSCI China is down by 5.8%. With the outlook for interest rates benign and President Trump appearing keen to do a deal with China before the 2020 elections, we continue to recommend investing in Equities and present our initial model portfolio below.

Fixed Income and FX markets

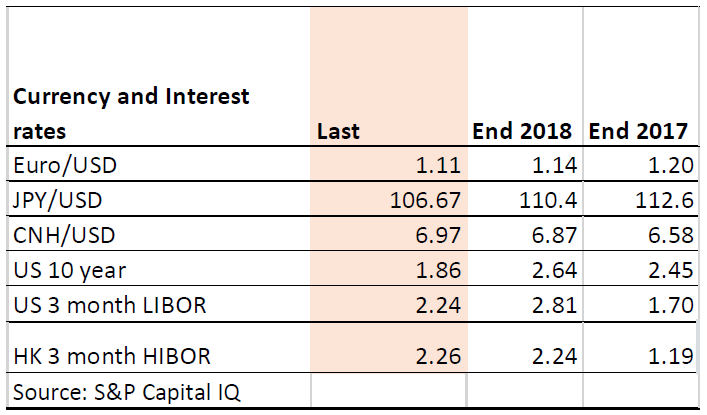

Since we last wrote Boris Johnson has assumed the position of UK Prime Minister, which has increased the chance of a hard Brexit. This has driven down the value of GBP and the Euro has also fallen as a hard Brexit would also cause economic damage to the EU. CNH and JPY has weakened marginally as investors prefer the USD. The Federal Reserve on Wednesday cut a key U.S. interest rate for the first time in 11 years. The target range for the federal funds rate has been reduced 25 bps to 2 to 2-1/4 percent. The market is expecting a period of economic weakness leading to further cuts of around 50 bps and the US 10 year Treasury yield has declined to 1.86% from 1.96% on July 5.

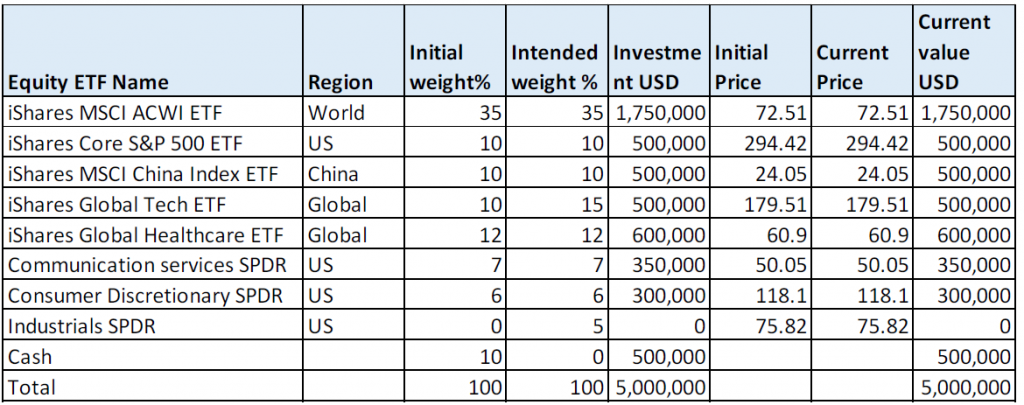

Equity ETF Model Portfolio

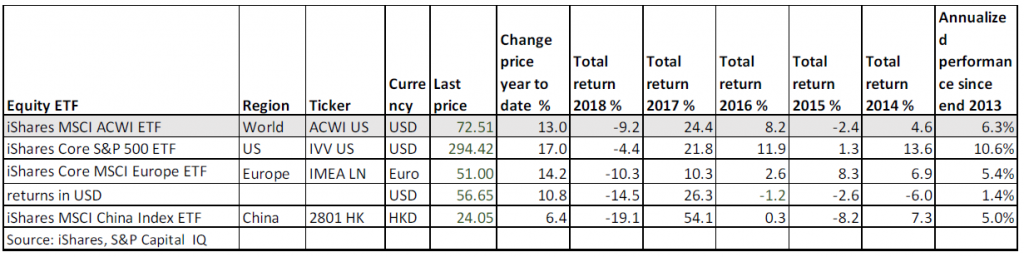

Above is the historic performance of the ETF tracking the global stock index as well as performance from the US, MSCI China and Europe ETF’s. This shows that amongst all the geographical sectors the US has been performing the best with a compound return of 10.6% per annum in the period since the end of 2013. MSCI China has been more volatile with a fantastic 54% return in 2017, followed by a poor 2018. Although it has rebounded in 2019 it has still lagged the US and Europe. The Europe ETF has underperformed (in USD terms) both China and the US. Based on i) the historic performance ii) the US has more companies that operate globally ( Apple, Alphabet, Amazon, Johnson and Johnson, Boeing, Coca Cola) iii) US is more stable in market downturn as most investment money comes from the US and there is home bias , I think that any equity portfolio should be overweight the US. Due to the relatively good value of MSCI China and that’s its capable of large rallies, I think that an equity portfolio for a China based investor should also be overweight in MSCI China.

When constructing a global portfolio using ETF we can also chose sector ETF. That way we can access good quality stocks in Europe and Japan, whilst avoiding the domestic banking sector which suffers from the political worries in Europe and the ageing population in Japan.

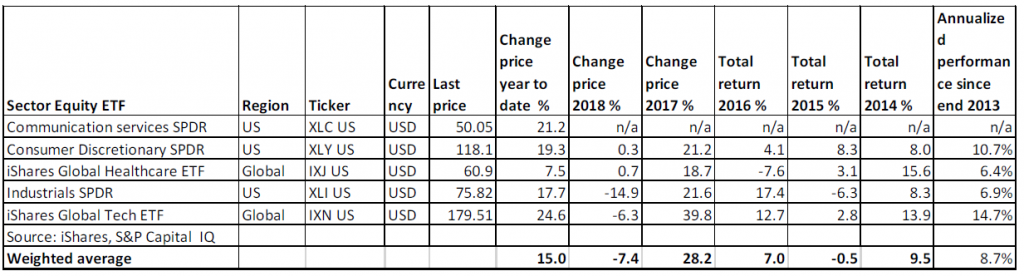

The Global Technology ETF has outperformed the Global Equity indices hugely and we recommend it. New and improved technology drive business productivity and consumer spending so leading Tech companies should continue to be strong investments in our view.

The Global Health Care ETF has been a moderate underperformer. Nevertheless, we still think it should be held as i) it provides good downside protection in the equity market down years of 2015 and 2018 ii) its a sector where companies are continually making new discoveries to boost profits iii) benefits from the aging population.

With regard to the US its also possible to invest through sectors rather than the ETF and we have chosen:

Communication Services: Seeks to provide precise exposure to companies from the media, retailing, and software & services industries in the U.S. The top three companies are Alphabet, Facebook and Activision Blizzard Inc. We consider this sector has strong growth potential both in the US and globally (because there are no global companies to rival Alphabet and Facebook)

Consumer Discretionary: The top three companies are: Amazon.com, Home Depot, McDonalds Corp, US has a competitive advantage in the Consumer space as it’s the worlds largest consumer market, this sector has outperformed most other US sectors since end 2013.

Industrial: The top three companies are: Boeing, Union Pacific Corporation and Honeywell International Inc, US Industrials should benefit from Trump policies, this sector is relatively volatile and experienced a large decline in 2018 as profits are relatively sensitive to the economic cycle.

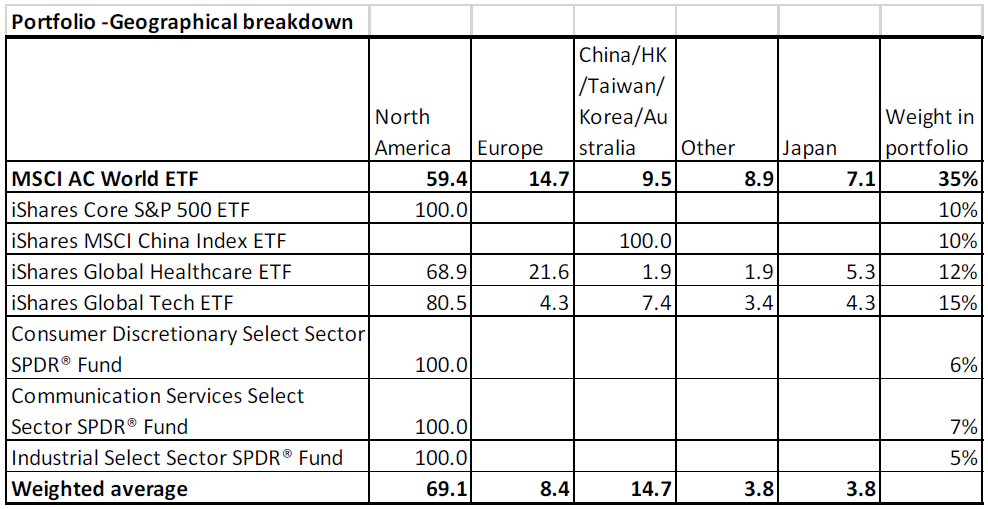

Risk Control: In order not to control risk relative to overall Global equities the portfolio is constrained to be not more than 10% over or underweight any geographical or sector area. Putting these ETF’s together we have allocated so as to achieve a 10% overweight to the US that is we hold 69% in the US whereas the allocation according to the MSCI AC world to North America would be 59%. We allocate 14.7% to the China economic influence area (including Asia ex Japan and Australia) vs a neutral 9.5% . Europe, Japan and other areas are underweight.

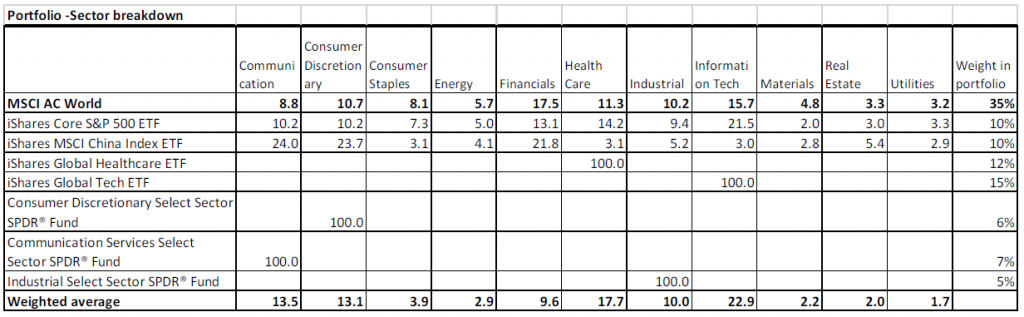

Analyzing by sector the portfolio is overweight: Communication by 4.7%, Consumer Discretion by 2.4%, health care by 6.4%, IT by 7.2% neutral Industrials and underweight other sectors.

In summary our recommended model portfolio is as laid out in the table below. Assuming that the portfolio was incepted at the end 2013 and in the period up to end 2018 the ishare S&P 500 was held instead of the US communication services ETF ( as it only started mid 2018) the model portfolio would have returned 8.7% p.a vs 6.3% p.a for the iShare on MSCI AC World.

In terms of timing we decide not to invest in the US Industrial sector at the moment due to expected economic weakness, also have decided to stagger investment into the Tech sector as its relatively high right now.