HKSFC Licensed Corp #ADC118

REVIEW OF 2019

October Newsletter

September 27, 2019

Ms. Z

January 28, 2020REVIEW OF 2019

REVIEW OF 2019

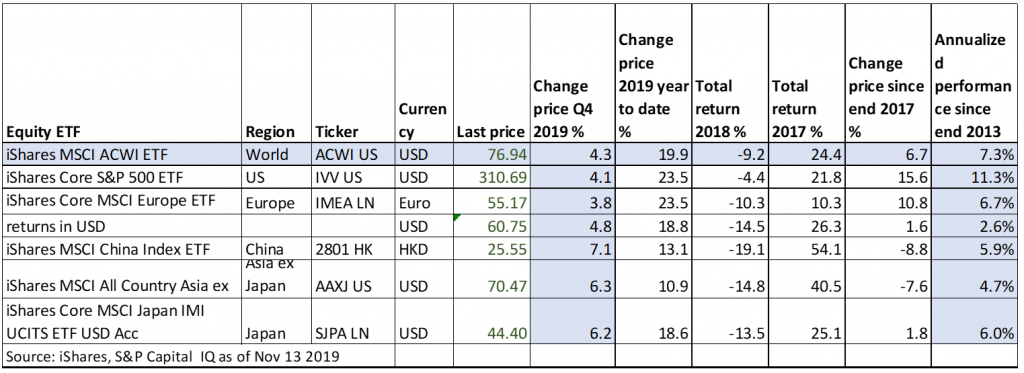

Equity market performance by region 2019

Global equity markets have done well in 2019 increasing by 19.9%. This has more than made up for the losses in 2018 with the gain since end 2017 being 6.7%. This has been led by the US, which is up by 23.5% this year and 15.6% since end 2017. China remains a laggard up by 13.1% this year but still down by 8.8% since end 2017. However, China has started to outperform in Q4 due to optimism on a US China Trade deal.

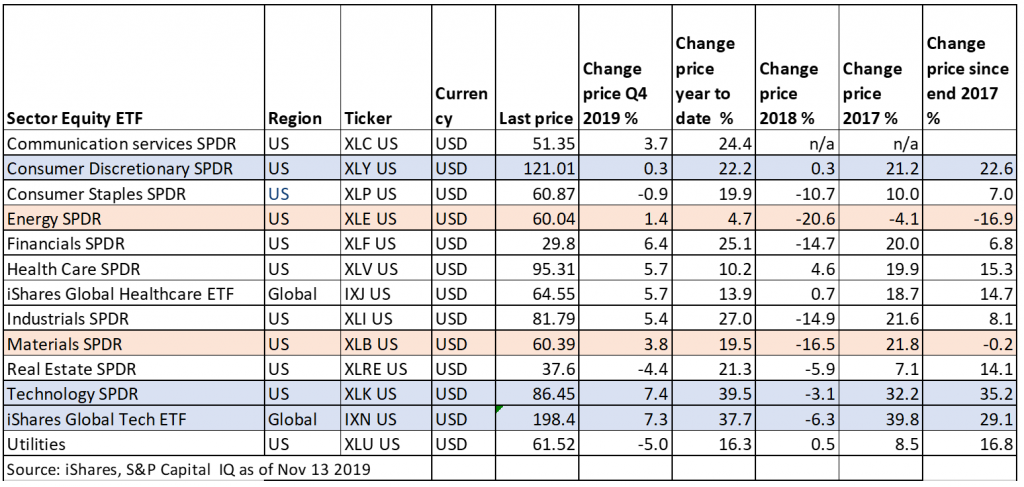

Equity market performance by sector 2019

By Sector Technology has outperformed on a short and long term basis and this is expected to continue. Consumer Discretion has also outperformed, up by 22.2% this year. This is largely due to the strong performance of Amazon. However, in Q4 the sector has underperformed as the Amazon share price consolidates. Energy and materials have been laggards, in line with the relative weakness of China. In Q4 Real Estate and Utilities underperformed as US 10 year yields are of their lows leading to bond proxies being out of favor.

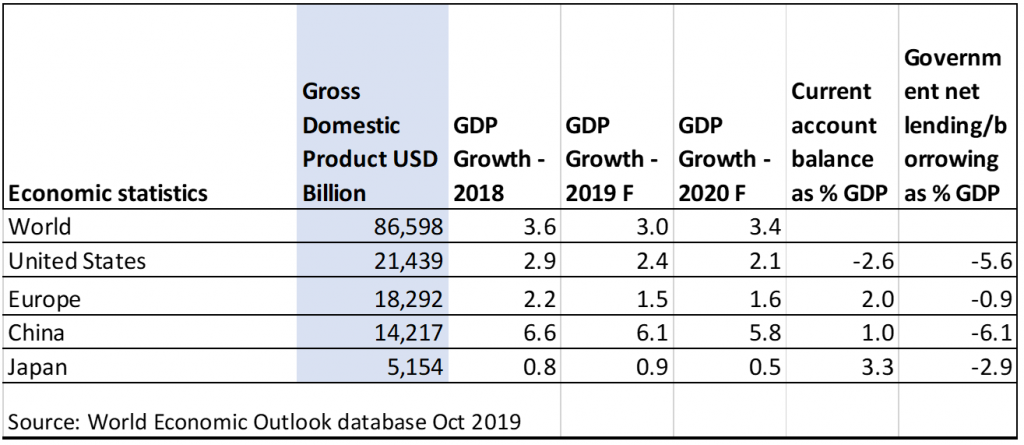

Economic snapshot

Economic growth has decelerated in 2019 vs 2018 across all regions, which is why interest rates have declined. In 2020 the IMF is expecting a further slowdown in GDP growth the US, China and Japan whereas Europe should stabilize at a low level.

In terms of Government and Current account balance Europe is relatively health – mainly due to the strong German economy. Despite the US China trade war, China is still expected to post a current account surplus in 2019.

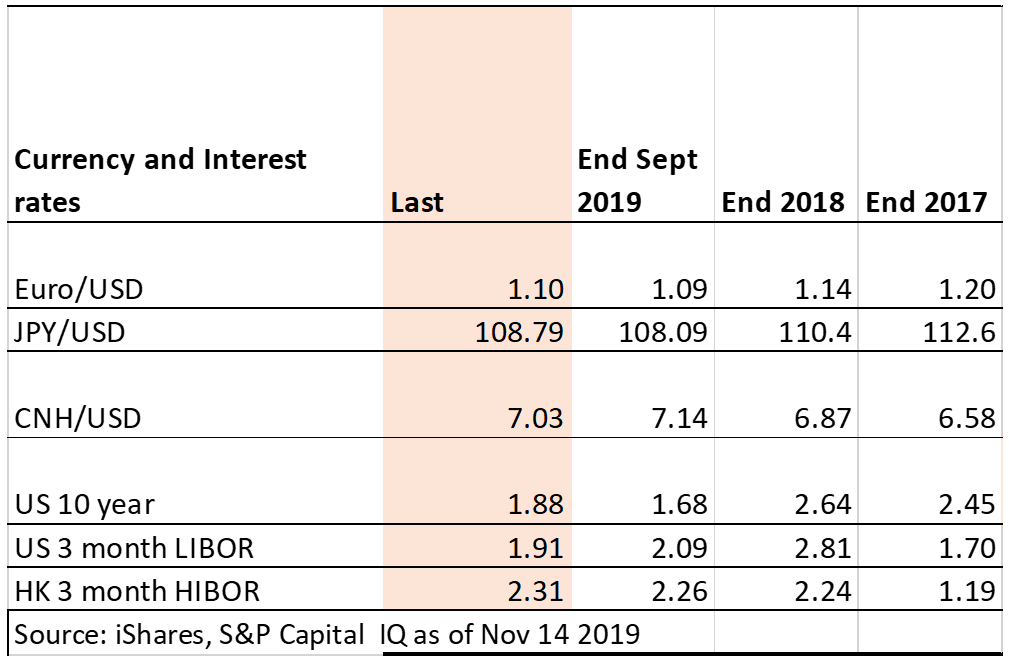

Currency and Interest rate snapshot

There has been a sharp reduction in interest rates in 2019, in response to the Fed cutting rates three times due to signs of slower growth in the US. However, the US 10 year treasury has rebounded of the low in Q4 as investors judge the scope for further interest rate cuts is limited

In response to a more bullish macro outlook and signs of a US China Trade deal the CNY has also rallied in Q4. Euro is also of the lows in Q4 as investors respond to more bullish macro outlook for 2020.

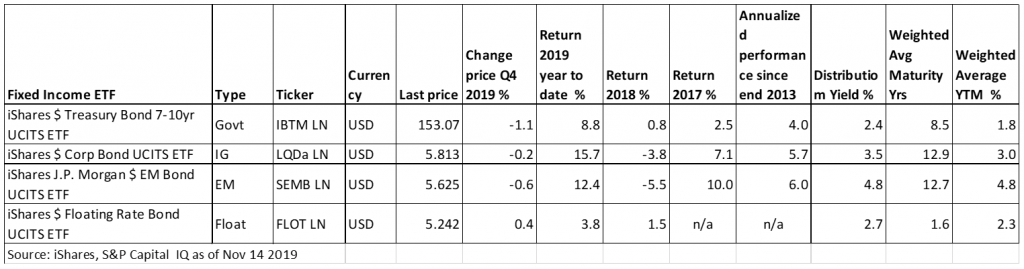

Fixed Income market performance 2019

In 2018 the increase in the US 10 Yr treasury yield and widening of credit spreads led to poor returns in Fixed Income space. In 2019 both trends were favorable leading to a sharp rally. As US 10 year has come of the low in Q4 2019, bonds have started the last quarter on a negative bias. Going forward prefer short duration and EM/High Yield credit.

Outlook 2020

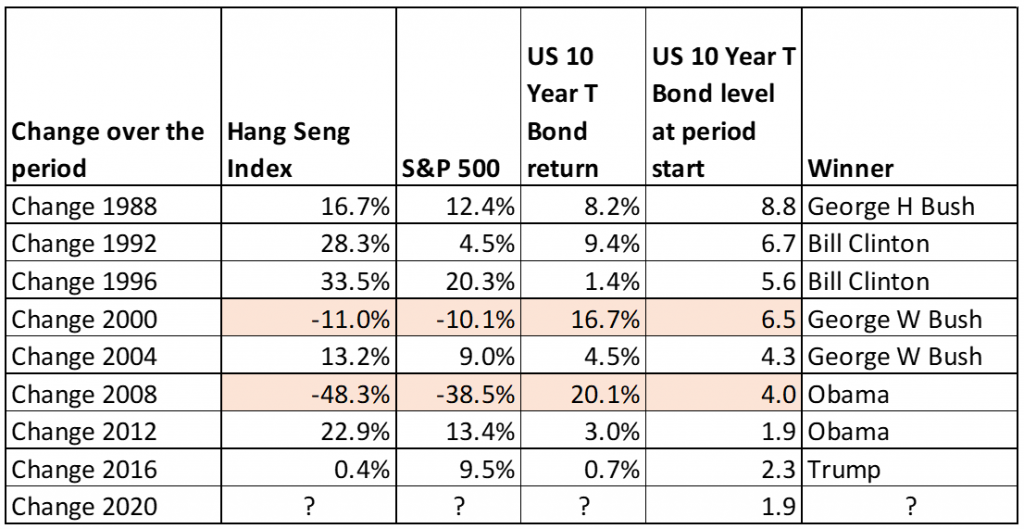

US presidential elections to take place 2020 – what can past election years teach us?

A US presidential election year has coincided with two very poor years for the Stock market being 2008 ( GFC) and 2000 ( Tech bubble ) – however, reasons for the decline may not be due to the election. Apart from these two years other Presidential election years saw positive returns for the US and Hong Kong markets and stable bond markets.

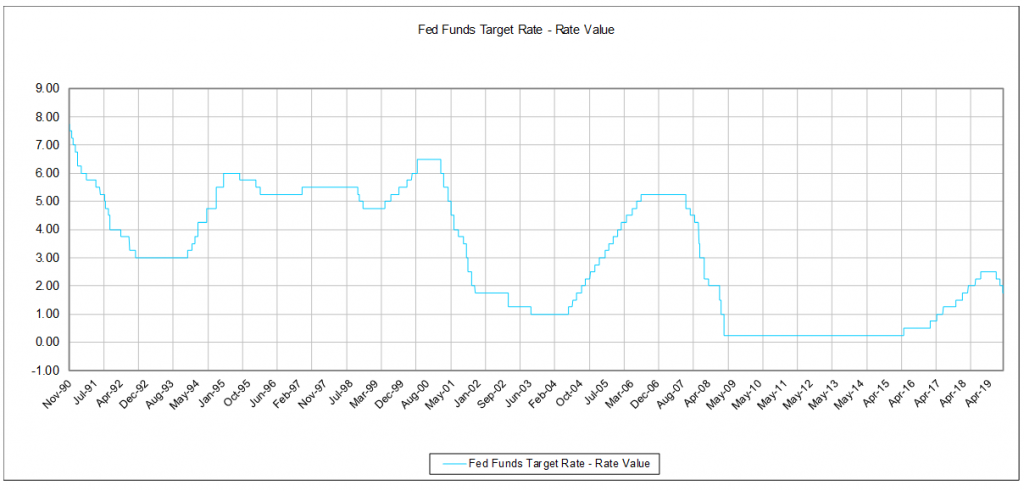

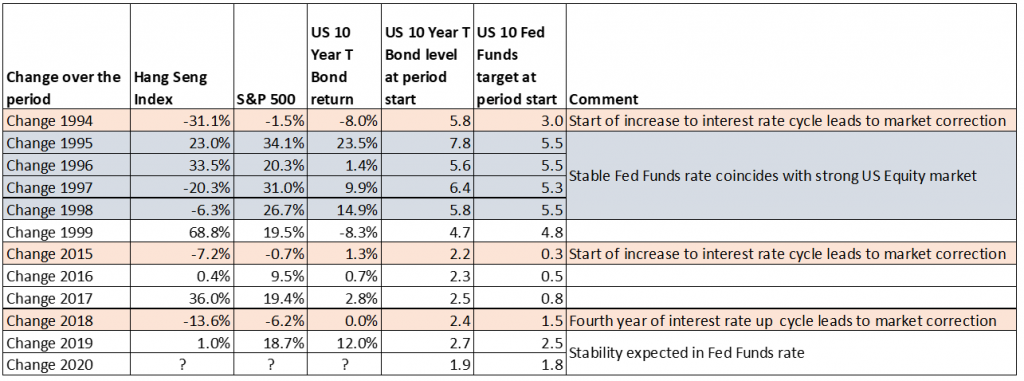

What happens after a mid cycle interest rate adjustment ?

In our view this series of interest rate cuts is a mid cycle adjustment – like 1995 and 1998 rather than part of a more sustained easing ( due to a weak economy) like 2000-2002 and 2008. If it is a mid cycle adjustment then then that means a relatively healthy economy , which is positive for the global equity markets. If it’s a sharp reduction in rates then that indicates a weaker than expected economy, which would be bad for equities.

Model portfolios

Asset allocation

We recommend an allocation to equities of between 20-50% depending on the Client’s need for Income. For Equity we recommend either the Axiom Global Sector Leaders portfolio or Axiom Global Equity ETF Portfolio. For Fixed Income we recommend : Emerging market for higher yield and Floating rate Bonds on basis that short term rates are close to the bottom

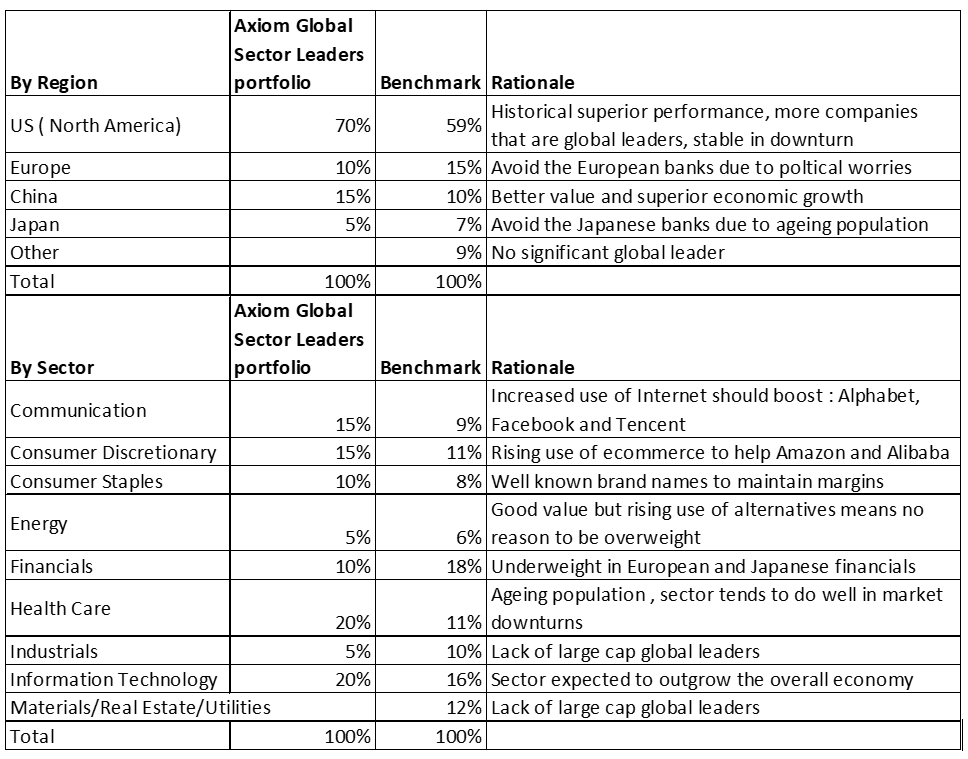

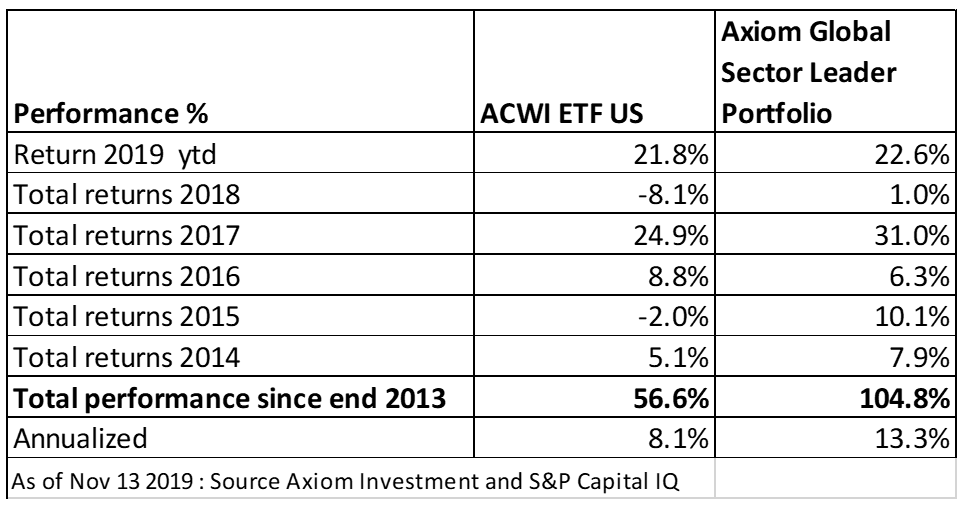

Axiom Global Sector Leaders portfolio review

From inception on August 14, 2019 to November 13, 2019, the Global Sector Leaders portfolio has delivered a return of 8.3% compared with the benchmark of 9.3%. The overweight to the leaders in the Information Technology sector such as Apple and Intel have added value. However, the overweight to Health Care and underweight in Financial services has detracted as Investors have bought into more cyclical sectors. Nevertheless, on the backtest the Axiom Global Sector Leaders portfolio has out performed convincingly – refer to the table below.

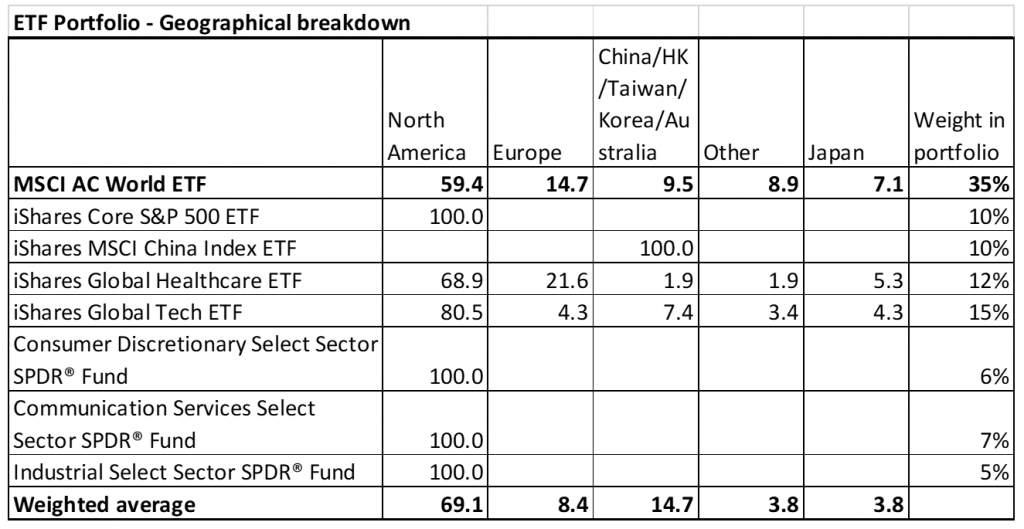

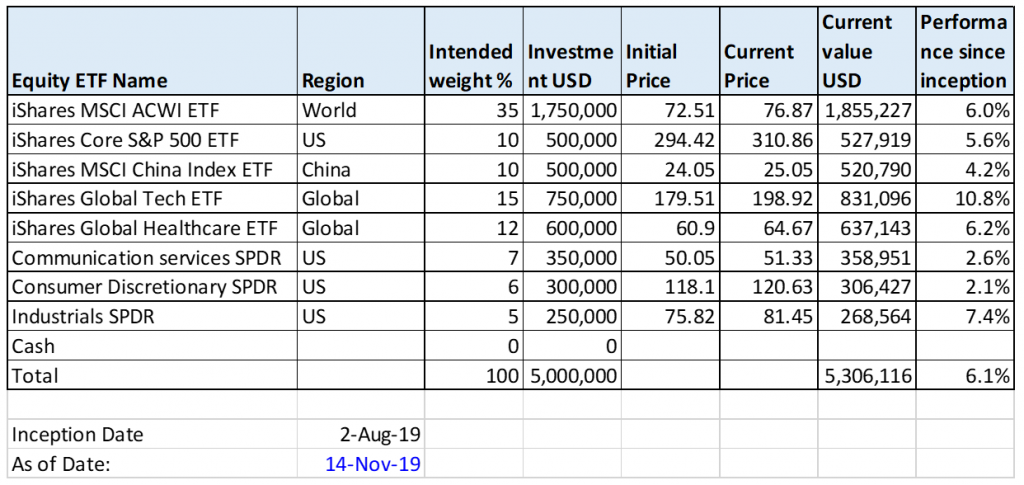

Axiom Global Equity ETF Portfolio review

An alternative method to construct a portfolio is to use ETF’s to get broad based stock exposure. That way the country and sector preferences can be expressed without taking any concentrated stock bets.

Since inception on 2 August 2019, the Axiom Global Equity ETF Portfolio has delivered a return of 6.1%. Amongst regions , Europe and Japan have outperformed . Amongst sectors Technology continues to outperform. Industrials also outperforming as investors hope the economic slowdown is temporary

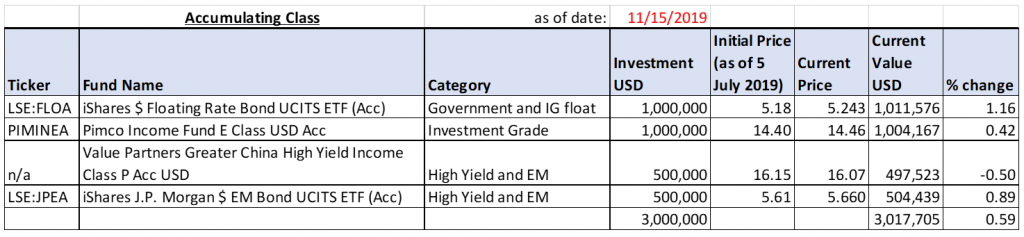

Axiom Bond Fund and ETF portfolio review

The portfolio has returned 0.58% since inception on 5 July 2019. It missed out on the rally in the 10 year Treasury by being short duration with the iShare on US Corp being up by 3.6 % and the iShare on 7-10 year Treasuries up by 2.3% over the period.

Going forward we don’t make any change to the model portfolio. We continue to prefer short duration – expressed through owning Floating rate iShare and PIMCO Income Fund. Value partners PRC High Yield has been underperforming but the underlying portfolio has a 12% yield to worst so is good value.

Philip Niem

All the information contained in this document is as of date indicated unless otherwise noted.

This document is issued by Axiom Investment Management Limited and has not been reviewed by the SFC. It may not be reproduced, distributed or transmitted to any person without express prior permission. This document and the information contained herein may not be distributed and published in jurisdictions in which such distribution and publication is not permitted.

Nothing contained here constitutes investment advice or should be relied on as such. The value of securities mentioned in the report and the income from it, if any, may fall or rise. Past performance of the securities mentioned in the report is not necessarily indicative of its future performance.

Axiom Investment Management Limited, 25/F, 168 Queen’s Road Central, Hong Kong. Telephone: 852 2537 2030 Facsimile: 852 2868-0091. Web: www.axiom-invest.com